Nobody enjoys writing a cheque to the CRA, but the good news is that Canada's tax code is full of legitimate ways to keep more of what you earn. If you live in Ontario, you're dealing with some of the highest combined marginal tax rates in the country - over 53% at the top bracket - so even modest planning can translate into real savings. Here's a practical rundown of the strategies that actually move the needle for most Ontario taxpayers.

Understand Ontario's Tax Brackets First

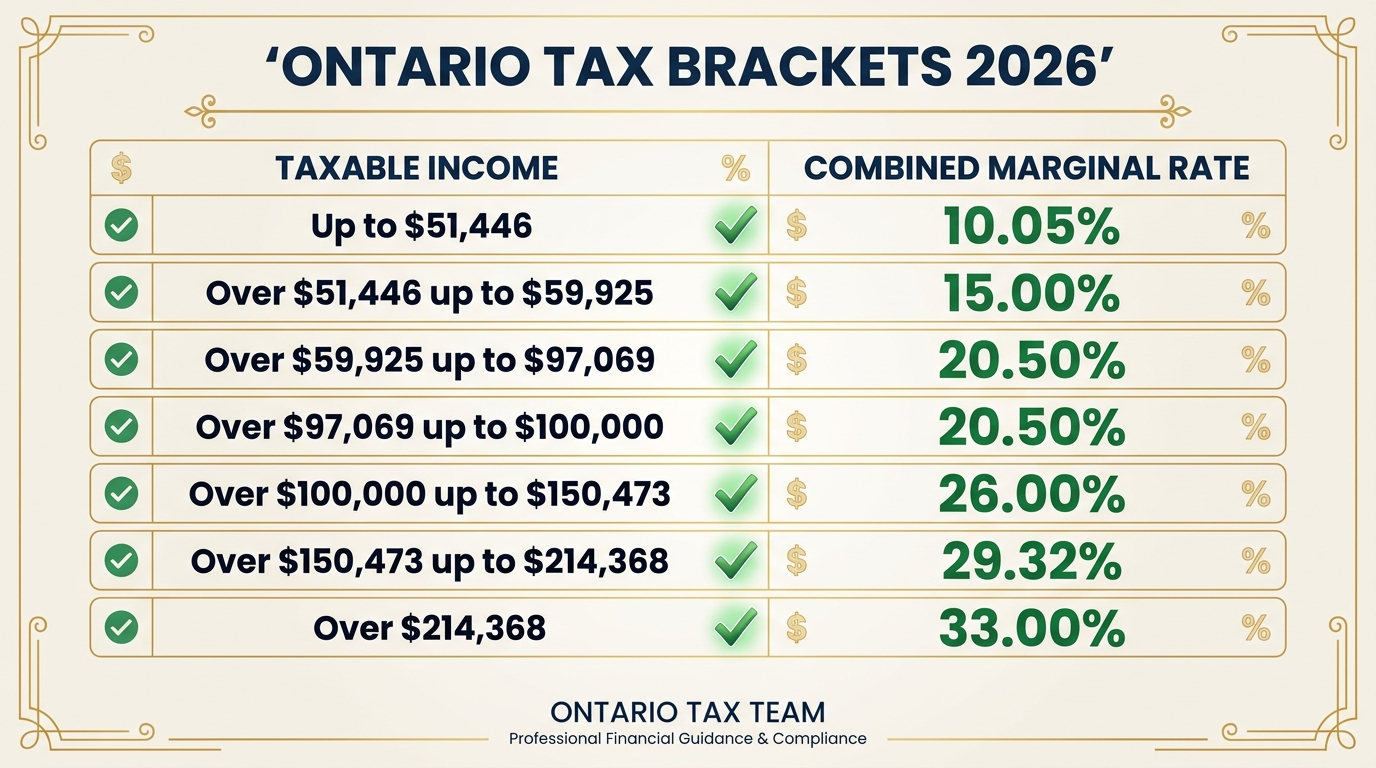

Before diving into tactics, it helps to know where you stand. Ontario uses a progressive system on top of the federal brackets. For 2025 (the tax year you're filing in spring 2026), the provincial rates range from 5.05% on the first $51,446 of taxable income up to 13.16% on income above $220,000. Combined with the federal rates, your marginal rate can climb past 53.53% once you cross the $235,675 threshold.

The practical takeaway: any dollar you can shift out of taxable income - through deductions or income splitting - saves you roughly half that dollar at the top bracket. Even at middle-income levels, marginal rates sit around 29% to 38%, so the savings are meaningful across the board. Try our Ontario tax calculator to see exactly where you fall.

Maximize Your RRSP Contributions

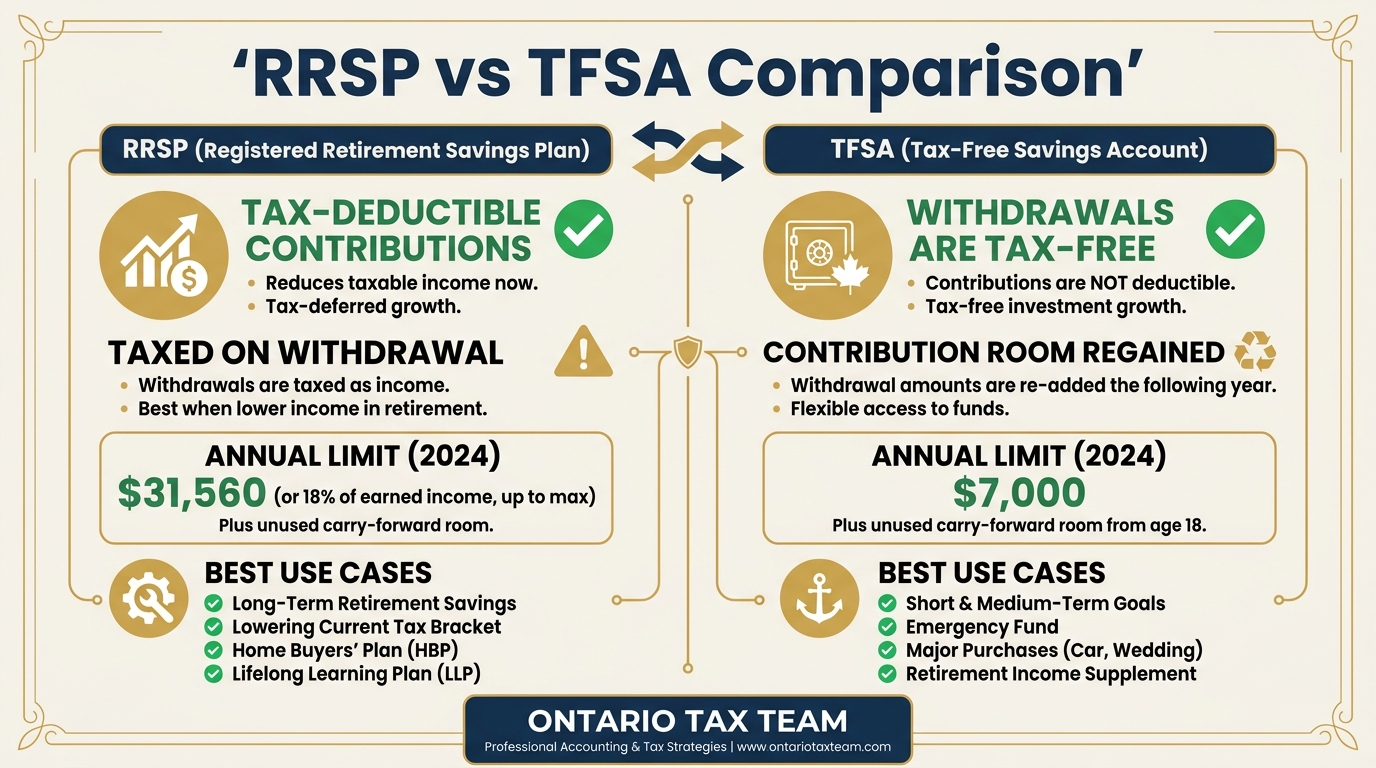

Registered Retirement Savings Plans remain the single most powerful tool for reducing your current-year tax bill. Every dollar you contribute comes directly off your taxable income, dollar for dollar. For the 2025 tax year, the contribution limit is 18% of your prior year's earned income, up to a maximum of $32,490 - see our full breakdown of the 2026 RRSP contribution deadline. If you didn't max out in previous years, that unused room carries forward indefinitely.

A few things people miss with RRSPs:

- You can contribute to a spousal RRSP and claim the deduction yourself, which helps shift future retirement income to a lower-income spouse

- You don't have to claim the deduction in the year you contribute - you can carry it forward to a higher-income year when the tax savings are greater

- The Home Buyers' Plan lets first-time buyers withdraw up to $60,000 from their RRSP tax-free for a home purchase, which you repay over 15 years

If you haven't been contributing regularly, talk to a tax planning professional about catch-up strategies using your accumulated room.

Use Your TFSA Strategically

The Tax-Free Savings Accountdoesn't give you a deduction when you contribute, but all the growth inside the account - interest, dividends, capital gains - is completely tax-free forever. The 2025 annual contribution limit is $7,000, and if you've been eligible since the TFSA launched in 2009, your total room could be over $95,000.

The tax savings here are indirect but powerful. Investment income that would otherwise be taxed at your marginal rate grows sheltered inside the TFSA. For Ontarians in the top bracket, that means every dollar of interest earned inside a TFSA would have cost you 53 cents in tax if held in a regular account.

Claim Pension Income Splitting

If you or your spouse receive eligible pension income, you can allocate up to 50% of that income to the lower-income spouse on your tax returns. This is done on the actual return - no money needs to physically move between accounts. Eligible pension income includes payments from a registered pension plan, RRIF withdrawals (if you're 65 or older), and certain annuity payments.

This is one of the most underused strategies for retired couples. Splitting $40,000 of pension income from a spouse in the 43% bracket to one in the 20% bracket can save over $9,000 in tax per year. If you're approaching retirement, your tax preparation should always include a pension-splitting analysis.

Don't Overlook Medical Expenses

The medical expense tax credit is broader than most people realize. Beyond the obvious - prescriptions, dental work, eyeglasses - it also covers:

- Travel costs over 40 km to access medical services not available locally

- Private health insurance premiums (if not deducted as a business expense)

- Certain home renovations for accessibility (wheelchair ramps, grab bars)

- Fertility treatments and surrogacy-related medical costs

- Service animals and related care costs

The credit kicks in once your eligible expenses exceed 3% of your net income (or $2,759, whichever is less). One tip: have the lower-income spouse claim medical expenses, since the 3% threshold is lower on a smaller income, letting you claim more.

Charitable Donations: The Two-Tier Credit

Canada's donation tax credit is structured as a two-tier system. The first $200 you donate earns a credit at the lowest marginal rate (about 20% combined in Ontario). Everything above $200 earns a credit at roughly 50% of the donation for high-income earners. So if you donate $5,000, the tax savings are approximately $2,440 - nearly half the donation comes back as a credit.

You can also carry forward unused donations for up to five years. If you make smaller donations throughout the year, consider pooling them into a single year to push past the $200 threshold and maximize the higher-tier credit. Couples should have one spouse claim all donations to consolidate past the first-tier amount.

Employment Expenses and Home Office Deductions

If you earn employment income and your employer requires you to pay for certain expenses, you may be able to deduct them on your personal income tax return using Form T777. Common deductions include home office costs(if you work from home more than 50% of the time), vehicle expenses for work-related travel, and supplies your employer doesn't reimburse.

You'll need a signed T2200 from your employer to claim these. The detailed method lets you deduct a portion of rent, utilities, internet, and maintenance based on the square footage of your workspace relative to your home.

Childcare and Family Credits

The childcare expense deduction allows you to deduct daycare, nannies, day camps, and boarding school fees up to $8,000 per child under 7 and $5,000 per child aged 7 to 16. This deduction must generally be claimed by the lower-income spouse, though exceptions exist for students and disabled individuals.

Ontario also offers the Ontario Child Care Tax Credit, which provides an additional refundable credit based on your family income. Don't forget the Canada Child Benefit - while not a deduction, it's calculated from your tax return, so filing accurately and claiming all deductions can increase your CCB payments.

Capital Gains Exemptions

If you own shares of a qualifying small business corporation, you may be eligible for the Lifetime Capital Gains Exemption, which shelters up to $1,016,836 (for 2025) of capital gains from tax when you sell those shares. For qualified farm or fishing property, the same exemption applies. This is a massive benefit that requires careful planning years before you sell. The shares must meet specific holding-period and asset tests, so getting professional advice early is essential.

There's also the principal residence exemption, which eliminates capital gains tax on the sale of your home. If you own rental property, the designation decision between your cottage and house needs careful analysis to minimize the total tax hit across both properties.

Put It All Together

The taxpayers who pay the least aren't doing anything exotic - they're just consistently using the tools the tax code already provides. Max out your RRSP. Fund your TFSA. Claim every medical expense and charitable receipt. Split pension income with your spouse. Deduct what your employer requires you to spend. These aren't loopholes; they're the system working as intended.

The key is doing this proactively, not scrambling in April. A comprehensive review of available deductions at the start of the year - or better yet, in the fall - gives you time to contribute to your RRSP, bunch charitable donations, and organize medical receipts before the filing deadline hits.

Key Takeaways

- •Ontario's top combined marginal rate exceeds 53%, making tax planning especially valuable for residents

- •RRSP contributions are dollar-for-dollar deductions - unused room carries forward indefinitely

- •Pension income splitting can save retired couples thousands annually with no cash transfer needed

- •Have the lower-income spouse claim medical expenses and pool charitable donations to maximize credits

- •Proactive planning throughout the year beats scrambling at tax time every time

Need Help Reducing Your Tax Bill?

Our team helps Ontario individuals and families save thousands through strategic tax planning. Book a free 15-minute consultation to review your situation.