Every year, the RRSP deadline sneaks up on people. You know it's coming, you mean to contribute earlier, and then suddenly it's late February and you're scrambling. For the 2025 tax year, the RRSP contribution deadline was March 3, 2026. If you missed it, that window is closed - but understanding how the RRSP works will help you plan better for next year and make the most of your existing contributions.

The 2026 RRSP Deadline: March 3, 2026

The rule is straightforward: you have 60 days after the end of the calendar year to make RRSP contributions that count toward the previous tax year. Since 2025 ended on December 31, the deadline fell on March 2 - but because that was a Saturday, the CRA extended it to Monday, March 3, 2026. Any contributions made between January 1, 2025 and March 3, 2026 can be deducted on your 2025 return.

Contributions made after March 3 still go into your RRSP, but they can only be deducted on your 2026 tax return (filed in spring 2027). So timing matters if you want the deduction this year.

Source: Canada Revenue Agency

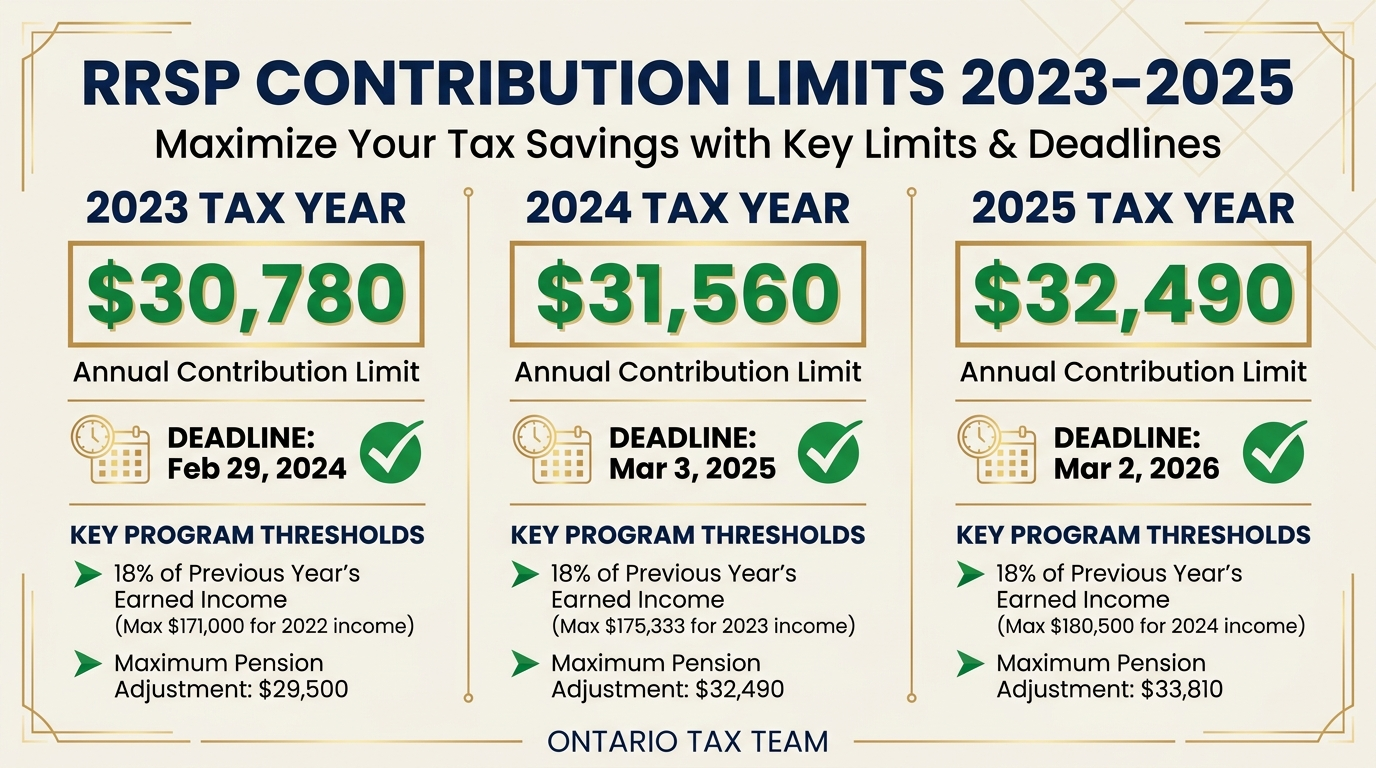

How Much Can You Contribute?

Your RRSP contribution limit (also called “deduction limit”) is based on 18% of your earned income from the previous year, up to the annual maximum. Here are the recent limits:

- 2024 tax year: $31,560 maximum

- 2025 tax year: $32,490 maximum

Your actual limit also factors in any pension adjustment (if you belong to a workplace pension plan) and any unused contribution room from previous years. The easiest way to check your exact limit is through your CRA My Account, on your most recent Notice of Assessment, or by calling the CRA's Tax Information Phone Service.

The key concept most people underestimate is unused room. If you earned enough to generate $32,490 in room but only contributed $10,000, the remaining $22,490 carries forward. Over several years, this accumulates. It's not uncommon for someone in their 30s or 40s to have $80,000 or more in unused RRSP room sitting there, waiting to be used.

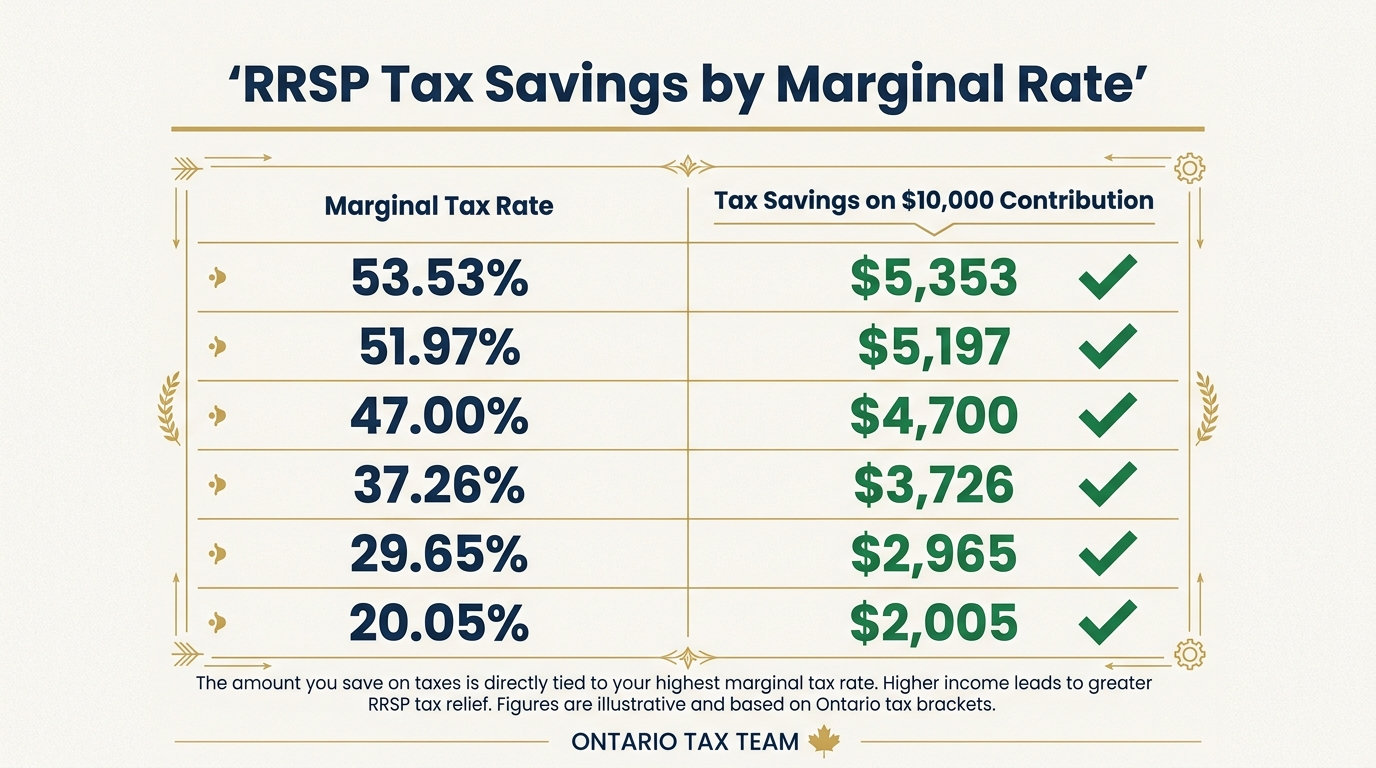

How RRSPs Actually Reduce Your Tax Bill

When you contribute to an RRSP, the amount comes directly off your taxable income. It's a deduction, not a credit, which means the tax savings scale with your marginal rate - use our tax calculator to find yours. If you're in a 43% combined bracket in Ontario and you contribute $10,000, you save $4,300 in tax. That money shows up as a bigger refund or a smaller balance owing when you file your personal income tax return.

The trade-off is that you'll pay tax when you eventually withdraw from the RRSP, typically in retirement. The bet is that your marginal rate will be lower in retirement than it is during your peak earning years. For most Canadians, that bet pays off handsomely. If you're self-employed, RRSP contributions are especially valuable since you have no employer pension plan.

A Quick Example

Sarah earns $95,000 in Ontario. Her combined marginal rate is about 38.5%. She contributes $15,000 to her RRSP before the deadline. Her taxable income drops to $80,000, and she saves roughly $5,775 in tax. When she withdraws that $15,000 in retirement at a marginal rate of 25%, she pays $3,750 in tax. Net lifetime savings: over $2,000 - plus decades of tax-sheltered investment growth on the original amount.

Spousal RRSPs: Income Splitting for Couples

A spousal RRSP lets you contribute to your spouse's RRSP and claim the deduction on your own return. The contribution uses your room, not theirs. The benefit is that when your spouse eventually withdraws the money, it's taxed in their hands at their (presumably lower) rate.

There's a three-year attribution rule to be aware of: if your spouse withdraws from the spousal RRSP within three calendar years of your last contribution, the withdrawal is attributed back to you and taxed at your rate. After three years, the income shifts cleanly to your spouse. This is a legitimate tax planning strategy that the CRA fully endorses when used properly.

The Home Buyers' Plan and Lifelong Learning Plan

Two special programs let you withdraw from your RRSP without immediate tax consequences:

- Home Buyers' Plan (HBP): First-time home buyers can withdraw up to $60,000 from their RRSP to purchase a qualifying home. You repay the amount over 15 years, starting two years after the withdrawal. If you miss a repayment, that amount is added to your taxable income for the year.

- Lifelong Learning Plan (LLP): You can withdraw up to $10,000 per year (to a maximum of $20,000) to fund full-time education for yourself or your spouse. Repayments begin five years after the first withdrawal or two years after leaving school, whichever is earlier.

Both programs are useful, but they work best when you have a clear repayment plan. The money you withdraw misses out on tax-sheltered growth, so it's worth calculating whether the withdrawal truly makes sense for your overall tax situation.

Over-Contribution Penalties

The CRA gives you a $2,000 lifetime over-contribution buffer. If you exceed your RRSP limit by more than $2,000, you'll face a penalty of 1% per month on the excess amount until you withdraw it or earn new room. This might not sound like much, but it adds up quickly - a $10,000 over-contribution costs $100 per month, $1,200 per year, until corrected.

Over-contributions usually happen when people don't check their actual room before contributing, especially if they have a pension adjustment they weren't aware of. Always verify your limit before making a large lump-sum contribution. This is one of the common tax filing mistakes we see every year.

What If You Missed the Deadline?

If you didn't contribute before March 3, 2026, you can still contribute any time during the year. Those contributions will count toward your 2026 deduction (or you can carry the deduction forward). The room you didn't use for 2025 doesn't disappear - it carries forward and adds to your 2026 limit. Make sure to prepare your documents for tax season so your contribution receipts are ready for filing.

The real cost of missing a deadline isn't lost room; it's a delayed tax refund. If you were counting on a refund to pay down debt or reinvest, that cash arrives a year later than it could have.

Plan Ahead for Next Year

The best RRSP strategy isn't a last-minute lump sum - it's automatic monthly contributions throughout the year. You benefit from dollar-cost averaging on your investments, and you don't have to scramble for a large sum in February. Even $500 per month adds up to $6,000 of tax-sheltered contributions by year-end. Also consider how RRSPs compare to TFSAs when deciding where to allocate your savings.

Key Takeaways

- •The RRSP deadline for the 2025 tax year was March 3, 2026 - contributions after that date apply to 2026

- •The 2025 contribution maximum is $32,490 (18% of prior year earned income), plus any unused room from prior years

- •RRSP deductions reduce taxable income dollar for dollar, with savings equal to your marginal tax rate

- •Spousal RRSPs, the Home Buyers' Plan, and the Lifelong Learning Plan offer additional flexibility

- •Over-contributions beyond the $2,000 buffer incur a 1% monthly penalty until corrected

Need Help With RRSP Tax Planning?

Our tax planning team helps you maximize RRSP contributions and reduce your tax bill. Book a free 15-minute consultation.