One of the most common questions Ontario business owners ask is: “Should I incorporate or stay a sole proprietor?” The answer depends on your income level, how much money you withdraw from the business, your growth plans, and your risk tolerance. Here's a detailed comparison to help you decide.

What Is a Sole Proprietorship?

A sole proprietorship is the simplest business structure. You and your business are the same legal entity. You report your business income on your personal tax return(T1) using the T2125 form. There's no separate legal entity, no corporate tax return, and minimal paperwork.

Advantages of Sole Proprietorship

- Simplicity: Easy and inexpensive to set up and maintain

- Low cost: No incorporation fees, annual returns, or corporate tax filings

- Personal tax credits: You can use business losses to offset other personal income

- Direct access to cash: All business profits are yours - no need to pay yourself a salary or dividends

Disadvantages of Sole Proprietorship

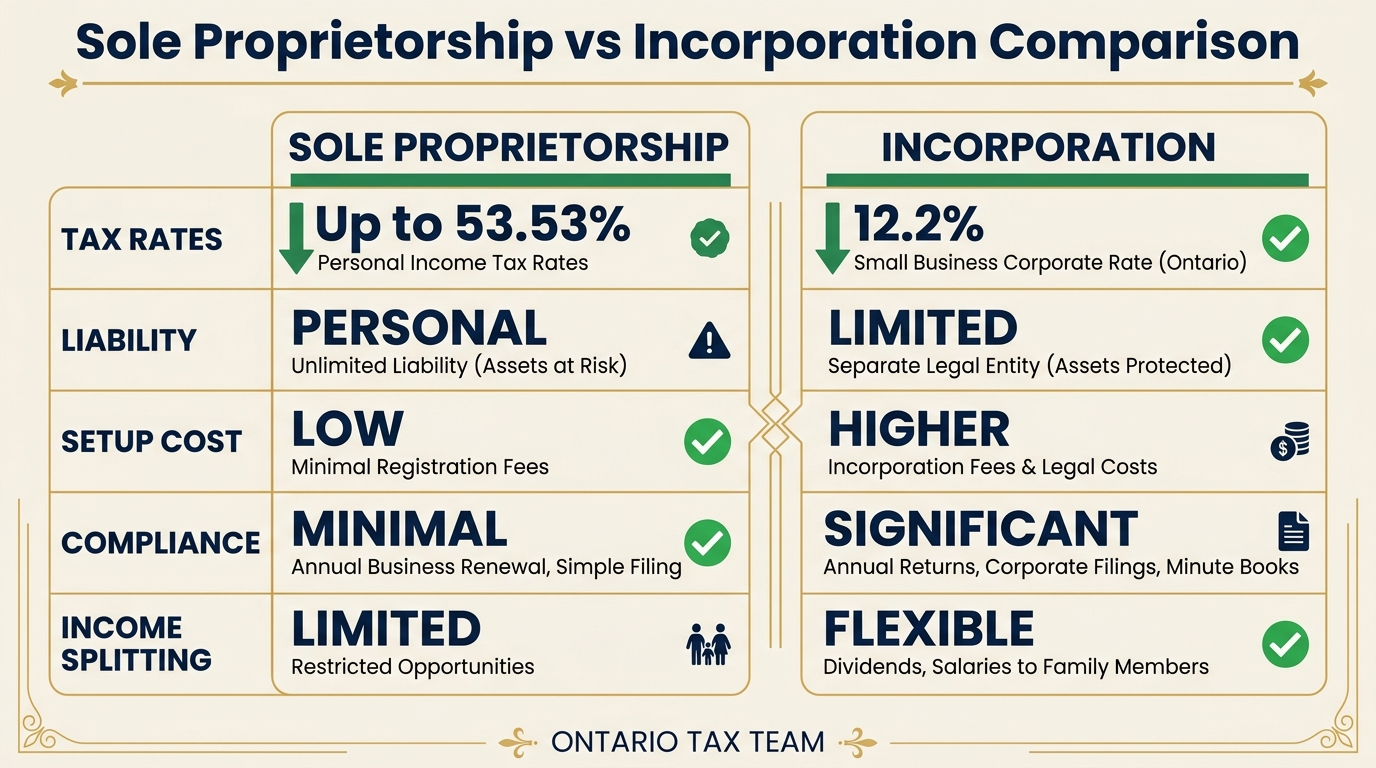

- Unlimited liability: You're personally liable for all business debts and legal claims

- Higher tax rates: All business income is taxed at personal marginal rates (up to 53.53% in Ontario)

- No tax deferral: You pay tax on all business income in the year it's earned, even if you don't withdraw it

- Limited income splitting: Fewer opportunities to split income with family members

What Is Incorporation?

When you incorporate, you create a separate legal entity - a corporation - that owns and operates your business. The corporation files its own tax return (T2) and pays corporate tax rates. You pay yourself from the corporation through salary, dividends, or a combination of both.

Our business incorporation service handles the full process from articles of incorporation to CRA account setup.

Advantages of Incorporation

- Lower tax rates: The small business tax rate in Ontario is 12.2% on the first $500,000 of active business income (compared to personal rates up to 53.53%)

- Tax deferral: Leave profits in the corporation and pay the lower corporate rate; you only pay personal tax when you withdraw funds

- Limited liability: Your personal assets are generally protected from business debts and legal claims

- Income splitting: Pay dividends to family members who are shareholders (subject to TOSI rules)

- Lifetime Capital Gains Exemption: Up to $1,016,836 (2026) on qualifying small business shares

- Credibility: Some clients and contracts require or prefer working with incorporated businesses

Disadvantages of Incorporation

- Setup costs: $1,000 to $2,500 for legal incorporation and initial setup

- Ongoing compliance: Annual corporate tax returns, annual filings, minute book maintenance

- Accounting costs: Corporate bookkeeping and tax filing typically costs $2,000 to $5,000+ per year

- No personal tax credits on corporate income: Business losses stay in the corporation and can't offset personal income

- Double taxation risk: Corporate profits are taxed at the corporate level, and again when withdrawn as salary or dividends (though the system is designed to integrate these)

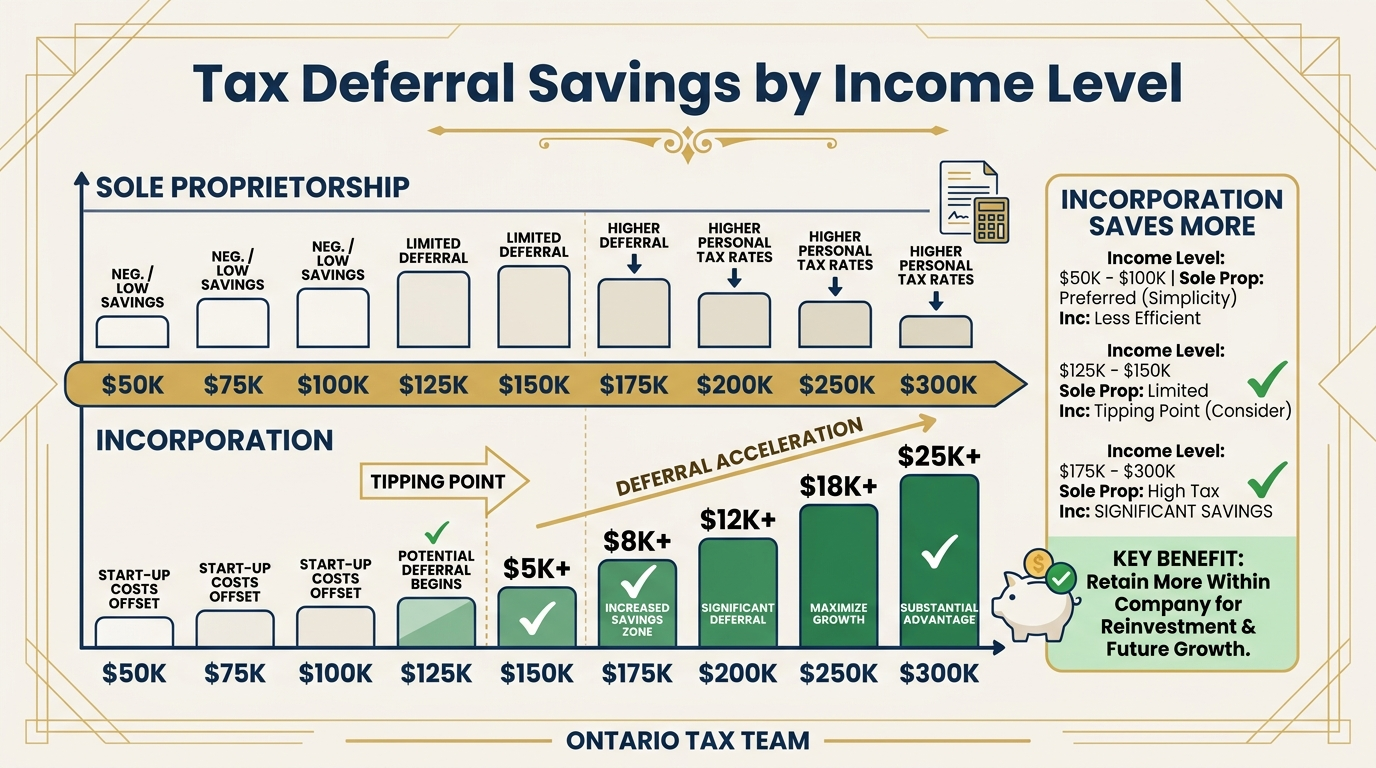

Tax Rate Comparison

Here's where the numbers make the biggest difference. In Ontario:

- Corporation (small business): 12.2% on the first $500,000

- Sole proprietor earning $100,000: Approximately 29.65% average tax rate

- Sole proprietor earning $200,000: Approximately 39.5% average tax rate

- Sole proprietor earning $300,000: Approximately 44% average tax rate

The gap between corporate and personal rates creates a significant tax deferral opportunity. If you earn $200,000 but only need $120,000 for personal expenses, the $80,000 left in the corporation is taxed at 12.2% instead of your marginal personal rate of 43.41%. Use our tax calculator to see how much you could save at your income level.

Our tax planning service models these scenarios for your specific income level.

When Should You Incorporate?

Incorporation typically makes financial sense when:

- Your net business income consistently exceeds $80,000 to $100,000 per year

- You don't need to withdraw all of your business income for personal expenses

- You want liability protection

- You plan to grow the business and reinvest profits - read more in our guide on when to incorporate your business in Ontario

- You want to build up investments inside the corporation

- You're planning for retirement and want to use the corporation as a savings vehicle

Read our guide on T1 vs T2 tax returns to understand the filing differences.

When Should You Stay a Sole Proprietor?

A sole proprietorship may be the better choice when:

- Your business income is under $80,000 per year

- You need to withdraw all business income for personal expenses

- Your business is new and may have losses in the early years (losses can offset personal income)

- You want to keep things simple and minimize compliance costs

- Your business has low liability risk

The Integration Factor

Canada's tax system is designed so that, in theory, you should pay roughly the same total tax whether you earn income personally or through a corporation. This is called “integration.” In practice, perfect integration doesn't always hold, and the real benefit of incorporation comes from tax deferral - paying less tax now and investing the savings inside your corporation.

Bottom Line

There's no one-size-fits-all answer. The right structure depends on your income level, cash flow needs, industry, growth plans, and personal financial situation. At Ontario Tax Team, we provide incorporation readiness assessments that analyze your specific situation and give you a clear recommendation. If you're earning over $80,000 and leaving money in the business, it's time to have the conversation. Book a free consultation with our business incorporation team or use our virtual accounting service from anywhere in Ontario.

Need Help Deciding Whether to Incorporate?

Our team provides incorporation readiness assessments for Ontario business owners, comparing your tax savings under each structure. Book a free 15-minute consultation.