If you operate an incorporated business in Ontario, you're required to file a T2 Corporation Income Tax Return with the CRA every year - even if the corporation had no income or was inactive. The T2 is more complex than a personal tax return, involving financial statements, multiple schedules, and GIFI codes that must all reconcile.

This guide walks you through the entire process, from understanding what's required to avoiding the penalties that catch many business owners off guard.

What Is a T2 Return?

The T2 Corporation Income Tax Return is the annual tax filing for all Canadian resident corporations. It reports the corporation's income, deductions, and tax payable for the fiscal year. Unlike the personal T1 return, which follows the calendar year, a T2 can cover any 12-month fiscal period the corporation has chosen.

For a deeper comparison between personal and corporate returns, see our guide to T1 vs T2 tax returns.

Who Needs to File a T2?

Every corporation resident in Canada must file a T2 return for each tax year, including:

- Active business corporations with revenue and expenses (including how to file a T2)

- Holding companies with investment income

- Inactive or dormant corporations (yes, even if there's no activity)

- Non-profit corporations incorporated under a corporate statute

- Tax-exempt corporations (they still file, but claim the exemption)

The only way to stop filing T2 returns is to formally dissolve the corporation through the provincial or federal corporate registry. As long as the corporation legally exists, the CRA expects a T2 every year. If you're considering whether to stay incorporated or switch to a sole proprietorship, understand these ongoing obligations.

Filing Deadlines

The T2 return is due six months after the end of the corporation's fiscal year. For example, if your fiscal year ends December 31, 2025, your T2 is due by June 30, 2026. If the year-end is March 31, the T2 is due by September 30.

However, the payment deadline is different - and this catches many business owners by surprise. Corporate tax payments are due:

- Two months after year-end for most corporations

- Three months after year-end for Canadian-controlled private corporations (CCPCs) that qualify for the small business deduction and had taxable income under $500,000 in the previous year

This means you may owe tax before your return is even due. Many corporations make instalment payments throughout the year to avoid a large balance at year-end. Our bookkeeping services help you track these obligations throughout the year.

What You Need to Prepare

Filing a T2 requires several components, all of which must be consistent with each other:

Financial Statements

You need a complete set of financial statements for the fiscal year, including an income statement (profit and loss), balance sheet, and statement of retained earnings. These form the foundation of the T2 - every number on the return traces back to the financial statements.

For most private corporations, a Notice to Reader (compilation) engagement is sufficient. Banks or investors may require a Review Engagement or Audit, which involves more work and higher fees.

GIFI Codes

The General Index of Financial Information (GIFI) is a standardized coding system the CRA uses to classify every line item on your financial statements. Every asset, liability, revenue, and expense account must be mapped to a GIFI code. Professional accounting software handles this mapping automatically, but if you're preparing your own statements, you'll need to assign codes manually - which is one of the most common sources of filing errors.

Tax Schedules

The T2 return includes numerous schedules that calculate specific components of your tax. The most commonly used schedules include:

- Schedule 1 - Net Income for Tax Purposes: Reconciles accounting income to taxable income by adding back non-deductible expenses and subtracting non-taxable items

- Schedule 8 - Capital Cost Allowance (CCA): Calculates depreciation deductions for assets like vehicles, equipment, computers, and leasehold improvements

- Schedule 100 - Balance Sheet: Reports assets, liabilities, and equity using GIFI codes

- Schedule 125 - Income Statement: Reports revenue and expenses using GIFI codes

- Schedule 200 - T2 Return itself: The main return that pulls information from all other schedules

- Schedule 3 - Dividends Received, Taxable Dividends Paid: Tracks inter-corporate dividends and dividends paid to shareholders

- Schedule 50 - Shareholder Information: Identifies all shareholders with 10% or more ownership

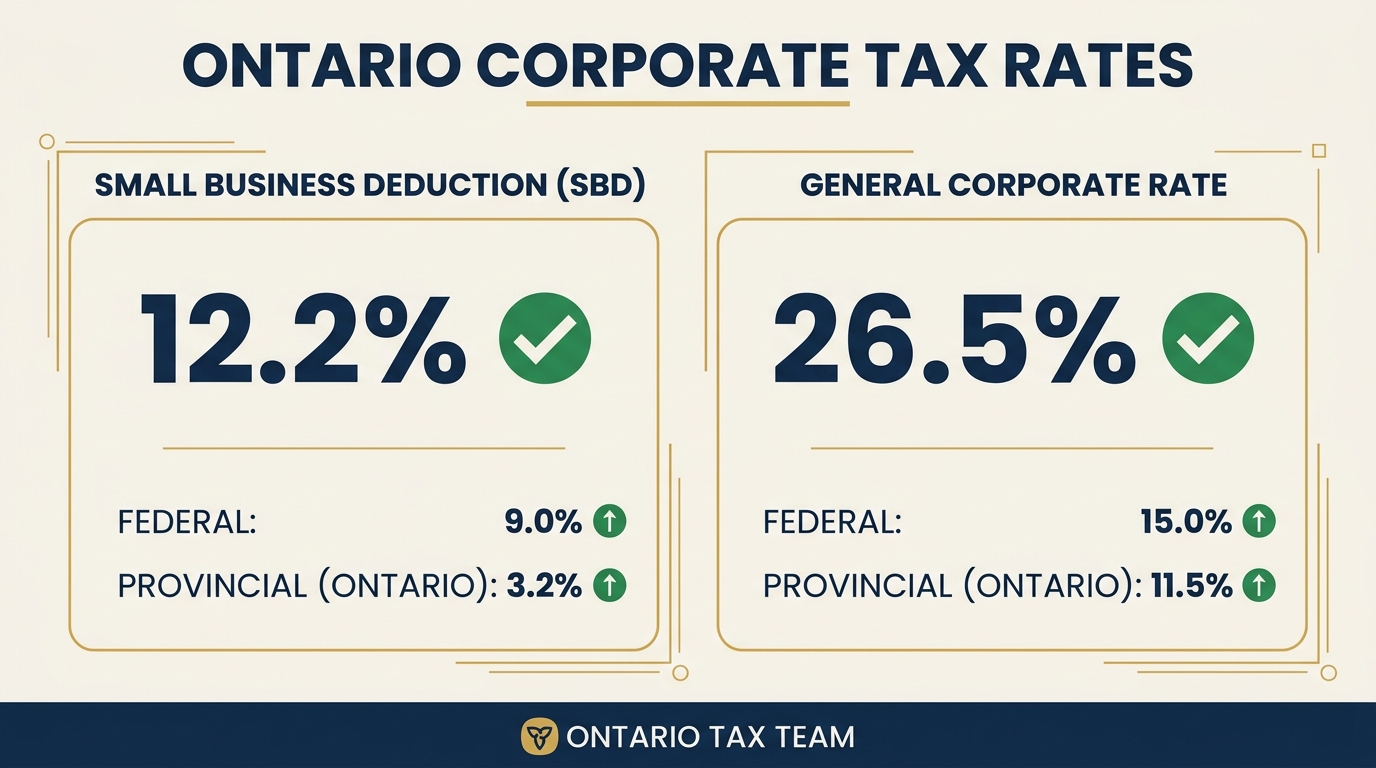

The Small Business Deduction

The small business deduction (SBD) is one of the most valuable tax benefits available to Canadian-controlled private corporations. It reduces the federal corporate tax rate on the first $500,000 of active business income from 15% to 9%. Combined with Ontario's small business rate of 3.2%, the total tax rate on qualifying income is just 12.2% - far lower than personal tax rates.

To qualify, your corporation must be a CCPC throughout the tax year, and there are clawback rules tied to taxable capital over $10 million and passive investment income over $50,000. For a complete breakdown, read our guide to the small business deduction in Canada.

Federal vs Provincial Corporate Tax

Ontario is one of the provinces that has a combined federal-provincial T2 filing. This means you file one return with the CRA that covers both federal and Ontario corporate tax. You don't file a separate provincial return unless you also have a permanent establishment in a province that isn't part of the federal filing agreement (Alberta and Quebec require separate provincial filings).

For Ontario corporations, the combined general corporate tax rate is 26.5% (15% federal + 11.5% provincial), and the combined small business rate is 12.2% (9% federal + 3.2% provincial). You can compare these rates against personal tax using our tax calculator.

Source: Canada Revenue Agency

Penalties for Late Filing

Late filing a T2 triggers a penalty of 5% of the unpaid tax, plus 1% per complete month the return is late, up to a maximum of 12 months. For repeat late filers (late in any of the three preceding years), the penalty doubles to 10% plus 2% per month, up to 20 months.

On top of penalties, the CRA charges compound daily interest on any unpaid balance from the payment due date (two or three months after year-end), not from the filing due date. This means interest starts accruing months before the return is even due.

Even if the corporation has no tax owing, failing to file can result in the CRA issuing arbitrary assessments, revoking the corporation's ability to file electronically, or flagging the corporation for compliance action.

E-Filing Requirements

Since 2024, most corporations are required to file their T2 returns electronically using CRA-certified software. The only exceptions are insurance corporations, non-resident corporations, and corporations reporting in functional currency. Paper filing when you're required to e-file results in a penalty of $100 for the first occurrence and $250 for subsequent occurrences.

Professional corporate tax preparation services always e-file through certified software, which also runs validation checks before submission to catch common errors.

Common Mistakes to Avoid

- Missing the payment deadline: Remember that tax is due 2-3 months after year-end, not when the return is due

- Inconsistent financial statements: The numbers in your schedules must tie exactly to your financial statements

- Incorrect GIFI mapping: Wrong codes cause CRA processing issues and potential reassessment

- Not filing for inactive corporations: Dormant corporations still need to file a T2 every year

- Forgetting shareholder loan reporting: Shareholder loans not repaid within one year of the corporation's year-end can be included in the shareholder's personal income - the salary vs dividends decision affects this

- Ignoring instalment requirements: If your corporation owes more than $3,000 in tax, you may be required to make quarterly instalments

Bottom Line

Corporate tax filing in Ontario is significantly more complex than personal tax filing. The interaction between financial statements, GIFI codes, tax schedules, and the various tax rates and deductions means there are many places where errors can occur. Working with an experienced corporate tax accountant ensures your return is filed correctly and on time, your tax liability is minimized through proper planning, and your corporation stays in good standing with the CRA.

Key Takeaways

- •Every Canadian corporation must file a T2 annually - even if inactive or with no revenue

- •The filing deadline is 6 months after year-end, but tax payment is due 2-3 months after year-end

- •The small business deduction reduces the combined federal-Ontario rate to 12.2% on the first $500,000 of active business income

- •Late filing penalties are steep and double for repeat offenders - always file on time

- •Most corporations are now required to e-file; paper filing triggers penalties

Need Help With Corporate Tax Filing?

Our corporate tax team handles T2 returns, financial statements, and CRA compliance for Ontario businesses. Book a free 15-minute consultation.