One of the most common questions business owners ask after incorporating is: “Should I pay myself a salary or dividends?” The answer isn't simple, because both options have distinct tax consequences, cash flow implications, and long-term planning considerations. In many cases, the optimal approach is a combination of the two. This guide breaks down the key differences and helps you figure out what makes sense for your situation.

The Concept of Integration

Canada's tax system is designed around a principle called integration. In theory, you should pay roughly the same total tax whether you earn income personally (as a sole proprietor, for example) or earn it through a corporation and then pay it out to yourself. The corporation pays corporate tax first, and then when you withdraw funds as salary or dividends, you pay personal tax - and the combined amount should approximate what you'd pay if you earned the income directly.

In practice, integration is imperfect. Small differences in tax rates, credits, and deductions create planning opportunities. That's why the salary-versus-dividend decision matters - and why it's worth getting right. Our tax planning service helps business owners model the best approach for their circumstances.

Paying Yourself a Salary

When your corporation pays you a salary, the payment works the same as any employer-employee relationship. The corporation deducts the salary as a business expense, which reduces its taxable income. You report the salary as employment income on your personal T1 return and pay personal income tax on it.

Advantages of Salary

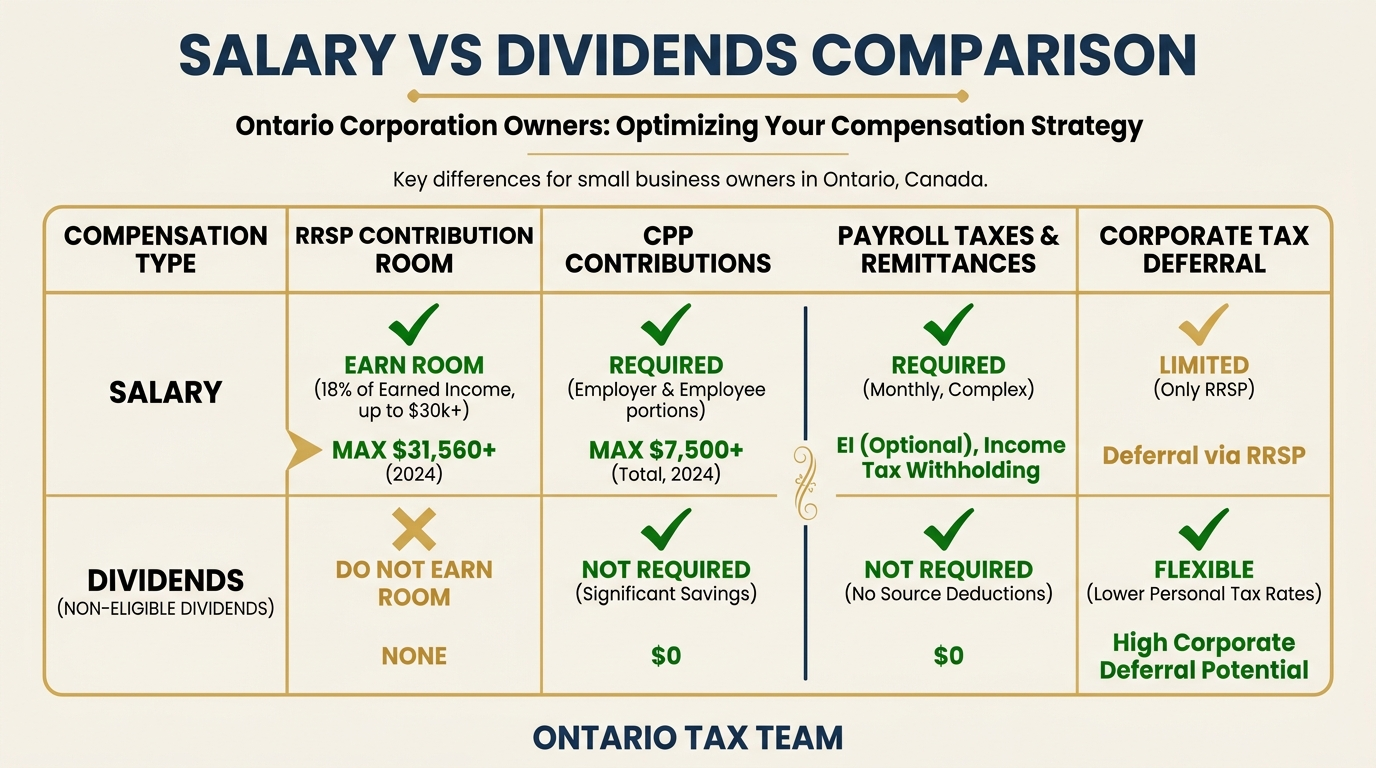

- RRSP contribution room: Salary creates earned income, which generates RRSP contribution room (18% of earned income, up to the annual maximum). Dividends do not create RRSP room. If you want to maximize your RRSP contributions, you need salary.

- CPP contributions: Salary triggers Canada Pension Plan contributions. While this is an additional cost (both the employer and employee portions), it builds your CPP retirement benefits. For many business owners, CPP provides a guaranteed stream of retirement income that supplements other savings.

- Deductible to the corporation: Salary is a deductible expense for the corporation, directly reducing its taxable income and the corporate tax it owes.

- Predictable personal income: A regular salary makes it easier to qualify for mortgages, lines of credit, and other personal financing. Lenders prefer consistent T4 income over variable dividend payments.

- Childcare expense deduction: If you claim childcare expenses, you need earned income. Dividends don't qualify as earned income for this purpose.

Disadvantages of Salary

- Payroll obligations: You must set up a payroll account with CRA, deduct income tax, CPP, and EI at source, and remit those deductions on schedule. Missing a payroll remittance deadline triggers penalties and interest quickly.

- CPP cost: In 2026, the combined employer-employee CPP contribution is significant. On maximum pensionable earnings, the total CPP cost (both portions) exceeds $8,000. As a business owner paying yourself, you effectively bear both sides.

- Higher immediate tax: Salary is taxed at your full marginal rate in the year you receive it. There's no deferral mechanism.

Paying Yourself Dividends

When your corporation pays dividends, the payment comes from after-tax corporate profits. The corporation does not get a deduction for dividends paid - it has already paid corporate tax on that income. You then report the dividend on your personal return, where it receives special tax treatment through the dividend gross-up and tax credit mechanism.

Advantages of Dividends

- No payroll remittances: Dividends are not subject to CPP, EI, or source deductions. There's no payroll account to manage, no remittance deadlines, and no T4 to file for dividends. You report them on a T5 instead.

- Tax deferral: Because the corporation pays tax at the small business rate (12.2% in Ontario on the first $500,000 of active business income), there's a substantial deferral advantage. Money left in the corporation is taxed at 12.2% instead of your personal marginal rate, which could be as high as 53.53%.

- Potentially lower effective rate: For certain income levels, the combined corporate tax plus personal tax on eligible dividends can be slightly lower than the personal tax on equivalent salary. This depends on your province and income level.

- Flexibility: You can declare dividends when it suits your tax situation - paying more in a low-income year and less in a high-income year.

Disadvantages of Dividends

- No RRSP room: Dividend income does not create RRSP contribution room. Over a career, this can mean hundreds of thousands of dollars in lost tax-sheltered savings.

- No CPP benefits: If you only take dividends, you won't contribute to CPP and won't receive CPP retirement benefits. You'll need to fund your entire retirement from other sources.

- Lending challenges: Some lenders don't fully recognize dividend income when assessing mortgage or loan applications, especially for non-eligible dividends from small businesses.

- Not deductible to the corporation: The corporation doesn't get a tax deduction for dividends, so the corporate tax on the underlying income is a real cost.

The Mixed Approach

Most tax professionals recommend a blended strategy. A typical approach is to pay yourself enough salary to maximize your RRSP contribution room (which requires about $175,000 in salary for the 2026 RRSP limit) and then take the remainder as dividends. However, the right mix depends on your specific situation.

For example, if you're in your 50s with a fully funded RRSP and no mortgage to qualify for, the RRSP room argument weakens. If you're 30, just bought a home, and want to build retirement savings, maximizing RRSP room through salary is much more valuable. Understanding the difference between T1 and T2 tax returns helps you see how personal and corporate taxes interact.

A Practical Example (Ontario, 2026)

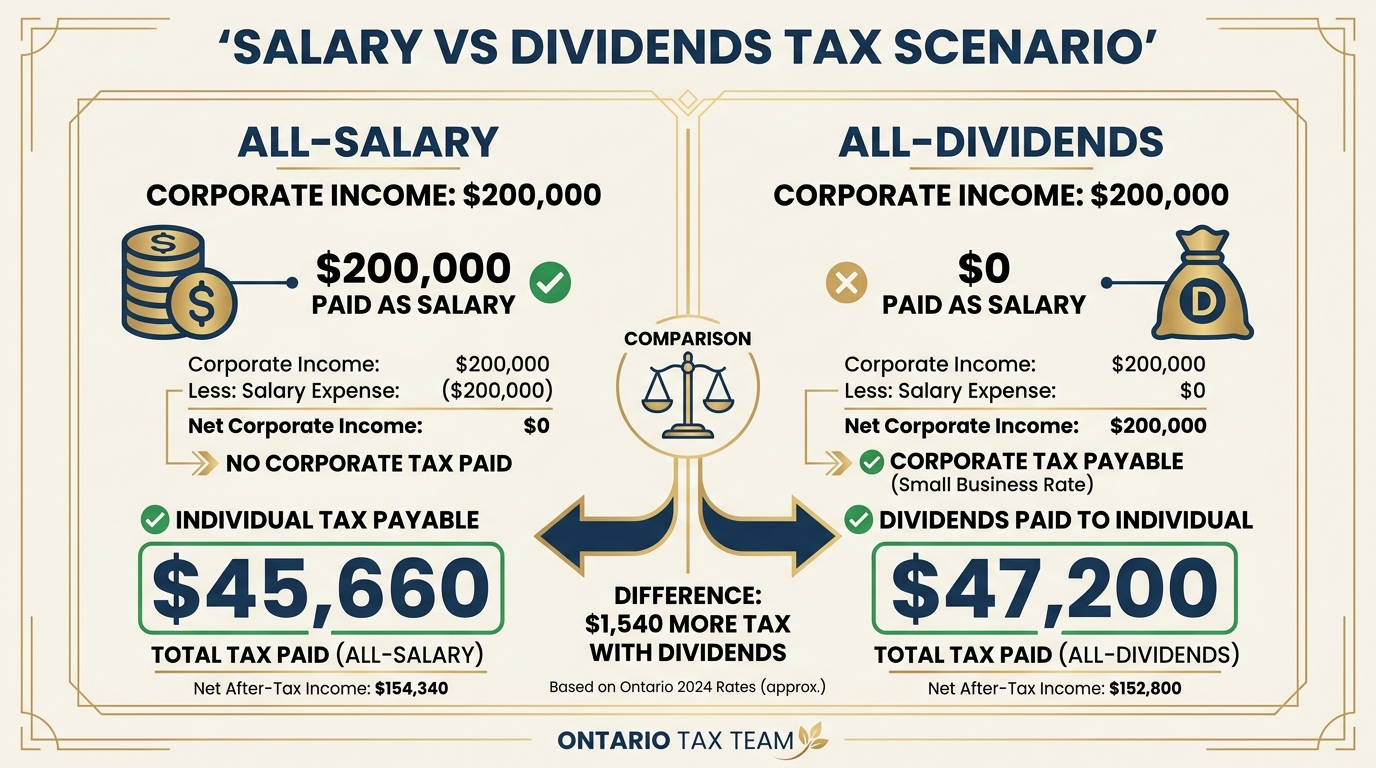

Suppose your corporation earns $200,000 in active business income. You need $120,000 for personal expenses. Here are two scenarios:

Scenario A - All Salary: The corporation pays you $120,000 in salary. Corporate taxable income drops to $80,000. The corporation pays about $9,760 in tax (12.2%). You pay personal tax on $120,000 in employment income - roughly $28,500 in combined federal and Ontario tax (after basic personal amounts). You also pay about $7,400 total in CPP contributions (employer and employee portions). Total tax: approximately $45,660. You generate about $21,600 in RRSP room.

Scenario B - All Dividends: The corporation pays tax on the full $200,000 at 12.2%, which is $24,400. That leaves $175,600 in after-tax corporate profits. You declare $120,000 in non-eligible dividends. After the gross-up and dividend tax credit, your personal tax on $120,000 in dividends is roughly $22,800. Total tax: approximately $47,200. No RRSP room generated. No CPP benefits.

In this example, the all-salary approach actually results in slightly lower total tax, plus you get RRSP room and CPP. But shift the numbers - higher income, lower personal spending needs - and the dividend route starts to win. This is exactly why professional corporate tax planning matters.

Tax on Split Income (TOSI) Rules

Before 2018, a common strategy was to pay dividends to family members (spouse, adult children) who were shareholders in the corporation, splitting income across lower tax brackets. The TOSI rules now heavily restrict this. Dividends paid to family members who are not actively engaged in the business (at least 20 hours per week) or who don't meet specific exemptions are taxed at the highest marginal rate, eliminating the benefit.

There are exceptions - for example, dividends to a spouse aged 65 or older, or to adult children who are genuinely involved in the business. But the rules are complex and the penalties for getting it wrong are severe. If you're considering income splitting, get professional advice. Understanding incorporation versus sole proprietorship is also helpful context for evaluating these strategies.

When to Choose Each Option

- Lean toward salary if: You want RRSP room, need CPP for retirement, are applying for a mortgage, have childcare expenses to deduct, or want a straightforward payroll setup.

- Lean toward dividends if: You want to minimize payroll administration, don't need RRSP room, have substantial other retirement savings, or want to defer tax by leaving profits in the corporation.

- Use a mix if: You want the best of both worlds - enough salary for RRSP and CPP, plus dividends for flexibility and deferral on the rest.

Bottom Line

The salary-versus-dividend decision is not one-size-fits-all, and it's not a decision you make once and forget. Your optimal mix should be revisited annually based on your income, expenses, tax bracket, retirement plans, and personal financial goals. A qualified accountant can model the scenarios, account for TOSI rules, and help you pay the least tax legally possible while building long-term wealth. For broader strategies, see our guide on reducing your personal taxes in Ontario.

Key Takeaways

- •Salary creates RRSP room and CPP benefits; dividends do not

- •Dividends avoid payroll remittances and offer tax deferral at the corporate level

- •A blended approach (salary plus dividends) is usually optimal for most business owners

- •TOSI rules restrict income splitting with family members - professional advice is essential

- •Revisit your salary-dividend mix annually as your situation changes

Need Help With Salary vs Dividend Planning?

Our corporate tax team models the optimal salary-dividend mix for your specific situation every year. Book a free 15-minute consultation.