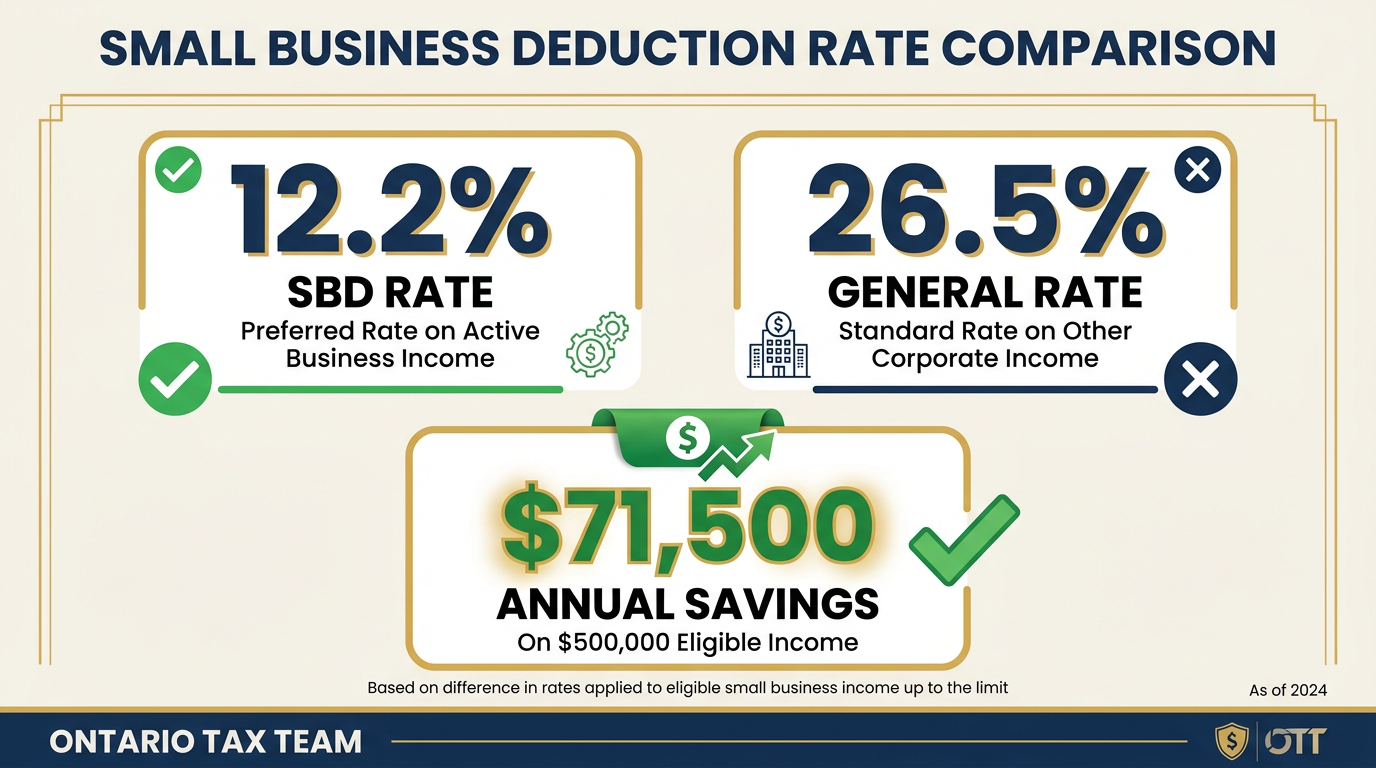

The Small Business Deduction is one of the biggest tax advantages available to Canadian-controlled private corporations. It reduces the federal corporate tax rate on the first $500,000 of active business income from 15% down to 9%, and when you add Ontario's small business rate of 3.2%, the combined rate comes to just 12.2%. That's a remarkable deal compared to the general combined corporate rate of 26.5% in Ontario. But qualifying for the SBD - and keeping it - involves rules that trip up a lot of business owners.

How the Small Business Deduction Works

At its core, the SBD is a tax rate reduction, not an actual deduction from income (the name is a bit misleading). It applies to active business income earned by a Canadian-Controlled Private Corporation (CCPC). “Active business income” means income from the corporation's operations - selling products, providing services, or carrying on a trade. It does not include investment income like interest, dividends, or rental income from property held as a passive investment.

The SBD reduces the federal tax rate from 15% to 9% on the first $500,000 of active business income. Combined with Ontario's provincial small business rate of 3.2%, the total tax on that income is 12.2%. On every dollar above $500,000, the corporation pays the general rate - 15% federal plus 11.5% provincial, totalling 26.5% in Ontario.

The difference is significant. On $500,000 of active business income, a corporation claiming the SBD pays $61,000 in tax. Without the SBD, that same income would generate $132,500 in tax. That's over $71,000 in annual savings - money that stays in the business for reinvestment, expansion, or compensation. Use our tax calculator to see the difference at your income level.

Source: Canada Revenue Agency

Who Qualifies: The CCPC Requirement

To claim the SBD, your corporation must be a Canadian-Controlled Private Corporation throughout the entire tax year. A CCPC is a private corporation incorporated in Canada that is not controlled directly or indirectly by non-residents or by public corporations. The key tests are:

- The corporation must be incorporated in Canada (federal or provincial incorporation both work)

- It cannot be controlled, directly or indirectly, by one or more non-resident persons

- It cannot be controlled by one or more public corporations

- No class of its shares can be listed on a designated stock exchange

Most small and medium-sized businesses incorporated in Ontario will meet these requirements without issue. Where it gets complicated is when there are multiple shareholders, holding companies, or cross-border ownership structures. If you're unsure about your CCPC status, a corporate tax professional can review your shareholding structure.

The $500,000 Business Limit and Associated Corporations

The $500,000 business limit must be shared among associated corporations. Two corporations are associated if one controls the other, or if the same person or group controls both. The classic scenario: you own Corporation A (a consulting firm) and Corporation B (a rental property holding company). If you control both, they're associated and must share the $500,000 limit between them.

This is a deliberate anti-avoidance measure. The government doesn't want business owners splitting their operations across multiple corporations just to multiply the SBD. The associated corporation rules cast a wide net, catching not just direct ownership but also family relationships and certain shareholder agreements.

Understanding whether your corporate structure involves association is critical for effective tax planning. Sometimes restructuring the ownership of related corporations can legitimately allocate the business limit more efficiently.

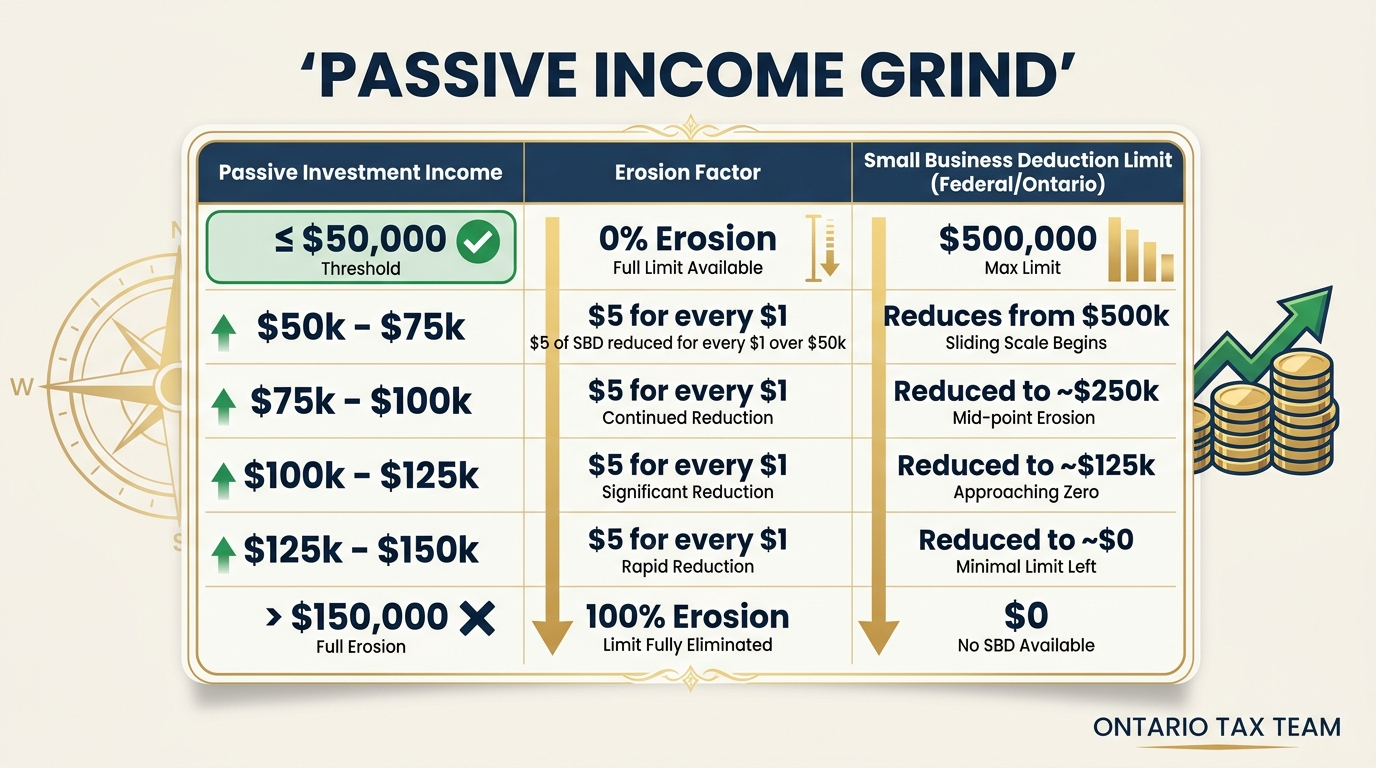

The Passive Income Grind

This is the rule that catches the most people off guard. Starting from 2019, if your corporation (and any associated corporations) earns more than $50,000 in aggregate investment income in the prior tax year, the $500,000 business limit starts to erode. For every dollar of investment income above $50,000, the business limit is reduced by $5. By the time your investment income reaches $150,000, the business limit is completely eliminated - and you lose the SBD entirely.

Let's walk through an example. Your corporation earned $400,000 in active business income and $80,000 in passive investment income (interest, dividends from portfolio investments, capital gains). Your prior-year investment income exceeded $50,000 by $30,000. That means your business limit is reduced by $150,000 (that's $30,000 multiplied by 5), dropping it from $500,000 to $350,000. The first $350,000 of your active income is taxed at 12.2%; the remaining $50,000 is taxed at 26.5%.

The policy rationale is straightforward: the SBD is meant to help small businesses reinvest in growth, not to subsidize passive investment portfolios held inside corporations. If you've been accumulating investments inside your corporation, this grind rule is something you need to actively manage. Strategies include paying out larger dividends or bonuses to keep investment income below the $50,000 threshold, or shifting passive investments into a separate holding company structure where the math works differently. Your bookkeeping records need to clearly separate active and passive income streams for this analysis.

Tax on Split Income (TOSI) Rules

The Tax on Split Income rules, often called the “kiddie tax” rules (though they now apply to adults too), can interact with the SBD in ways that affect how you extract income from your corporation. TOSI applies the top marginal tax rate to certain dividends and other income paid to family members who aren't actively involved in the business.

Before 2018, a common strategy was to pay dividends to adult children or a spouse who held shares in the corporation, taking advantage of their lower personal tax rates. The expanded TOSI rules now require that the family member meet specific “excluded amount” tests - generally based on the nature and extent of their involvement in the business, their age, and their capital contributions.

While TOSI doesn't directly reduce your SBD, it limits how efficiently you can distribute the after-tax corporate income that the SBD helped you preserve. Planning around TOSI usually involves ensuring that family members who receive dividends have genuine roles and contributions to the business, and that the amounts paid are reasonable relative to those contributions. This is an area where the incorporation vs sole proprietorship analysis becomes particularly relevant.

When Does the SBD Make Sense?

The SBD is most valuable when your corporation earns active business income that you don't need to withdraw immediately. The 12.2% corporate rate leaves 87.8 cents of every dollar available for reinvestment. If you extract that money as salary or dividends, you'll eventually pay personal tax on it - but deferring that personal tax while the money compounds inside the corporation is the real advantage.

The SBD is less valuable (or even irrelevant) if:

- You withdraw all corporate income as salary each year (the SBD rate doesn't matter if nothing stays in the corporation)

- Your passive investment income exceeds $150,000, eliminating the SBD entirely

- Your business limit is shared across many associated corporations, leaving each one with a thin slice

- You're considering selling the business - the interplay between corporate and personal tax on the sale needs careful modeling

Plan With the Full Picture

The SBD doesn't exist in isolation. It interacts with the passive income grind, TOSI, the general rate income pool (GRIP), the capital dividend account, and the lifetime capital gains exemption. Optimizing your tax position means looking at all of these together - not just minimizing corporate tax, but minimizing total tax across your personal and corporate returns combined. Our corporate tax filing guide for Ontario explains how these pieces fit together.

That's the kind of analysis that pays for itself many times over when done by someone who understands the full picture.

Key Takeaways

- •The SBD reduces the combined Ontario corporate tax rate to 12.2% on the first $500,000 of active business income

- •Only Canadian-Controlled Private Corporations qualify, and associated corporations must share the $500,000 limit

- •Passive investment income above $50,000 erodes the business limit at a rate of $5 per $1, fully eliminated at $150,000

- •TOSI rules limit income splitting with family members who aren't actively involved in the business

- •The SBD is most valuable when corporate income is retained for reinvestment rather than immediately withdrawn

Need Help Optimizing Your Small Business Deduction?

Our corporate tax team ensures your corporation maximizes the SBD and manages passive income thresholds. Book a free 15-minute consultation.