If you've sold an investment property, stocks, or a business, you've likely triggered a capital gain - and with it, a tax obligation. Use our tax calculatorto estimate what you might owe. Capital gains tax is one of the most misunderstood areas of Canadian tax law, yet it affects nearly everyone who owns assets outside of a registered account. Whether you're a real estate investor, a business owner selling shares, or someone who just sold a cottage, understanding how capital gains work can save you thousands of dollars.

What Is a Capital Gain?

A capital gain occurs when you sell a capital property for more than you paid for it. Capital property includes real estate (other than your principal residence), stocks, bonds, mutual funds, cryptocurrency, and business assets. The gain is the difference between your proceeds of disposition (selling price) and your adjusted cost base (what you paid, plus eligible expenses).

It's important to note that not all increases in value are capital gains. For example, if you buy and sell goods as part of a business, those profits are considered business income, not capital gains. The distinction matters because capital gains receive preferential tax treatment compared to regular income.

The Inclusion Rate: 50% and the 2025 Changes

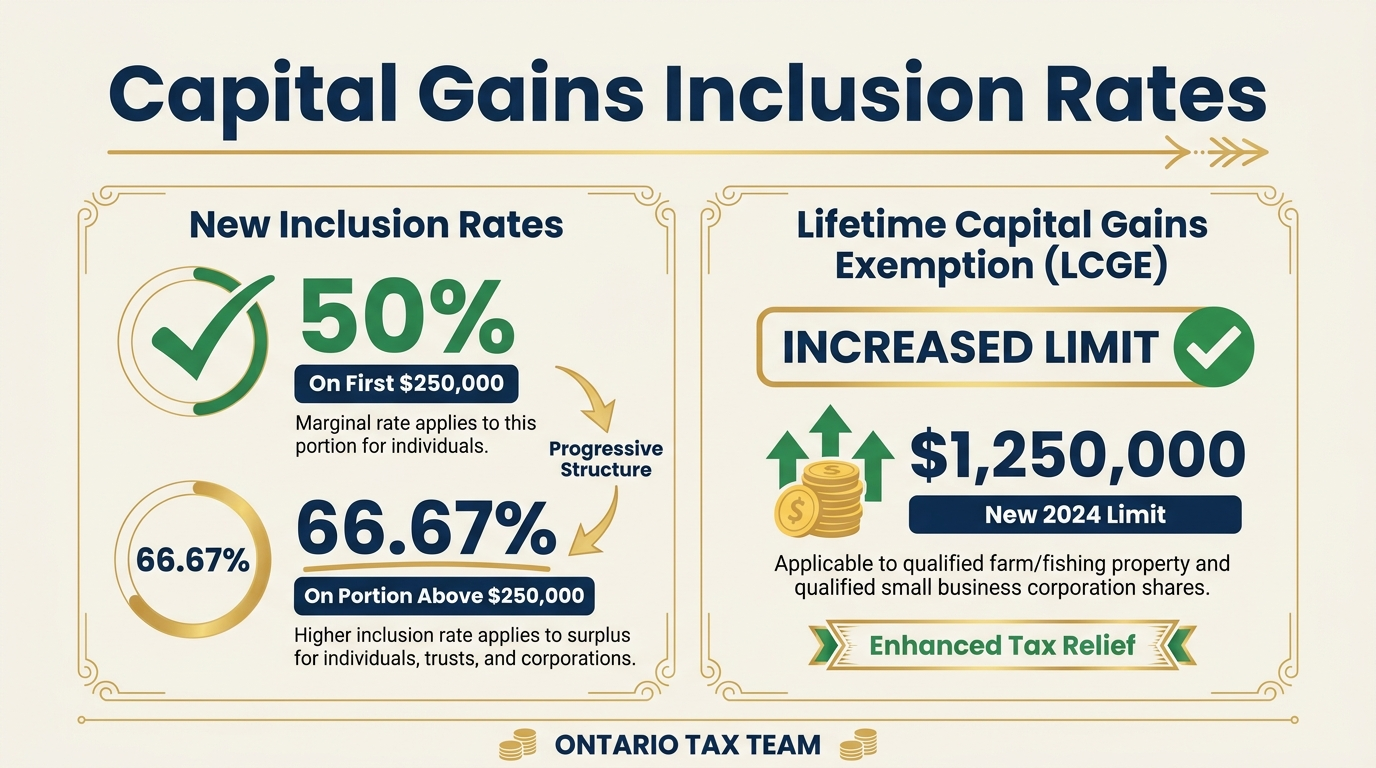

Historically, Canada has taxed only 50% of capital gains - meaning if you realize a $100,000 gain, only $50,000 is added to your taxable income. This 50% inclusion rate has been in place since 2000 and remains one of the more favourable tax treatments available to Canadian taxpayers.

However, beginning June 25, 2025, the federal government introduced a significant change: for individuals, the inclusion rate increases to 66.67% (two-thirds) on the portion of annual capital gains exceeding $250,000. The first $250,000 in net capital gains each year still benefits from the 50% inclusion rate. For corporations and trusts, the 66.67% rate applies to all capital gains, with no $250,000 threshold.

This change has meaningful implications for anyone selling high-value assets. If you're planning a significant disposition, working with a tax planning professional is essential to understand how the new rules affect your situation.

Practical Example

Suppose you're an individual who sells shares and realizes a $400,000 capital gain in 2026. Under the updated rules, the first $250,000 is included at 50% ($125,000 taxable), and the remaining $150,000 is included at 66.67% ($100,005 taxable). Your total taxable capital gain is $225,005 - compared to $200,000 under the old rules. At a combined marginal rate of roughly 48% in Ontario, that's about $12,000 in additional tax.

Source: Department of Finance Canada, 2024 Federal Budget

Calculating Your Adjusted Cost Base (ACB)

Your adjusted cost base is the original purchase price of the asset plus any costs you incurred to acquire it - legal fees, commissions, and transfer taxes. For real estate, you can also add the cost of capital improvements (a new roof, a renovation that adds value), but not routine maintenance or repairs.

For publicly traded securities, tracking your ACB can get complicated if you've made multiple purchases at different prices. In that case, you need to calculate the average cost per share across all your purchases. Most brokerages provide this information, but it's your responsibility to verify it at tax time. Proper bookkeeping of your investment transactions makes this far easier.

Reporting Capital Gains on Schedule 3

Capital gains and losses are reported on Schedule 3 of your personal income tax return(T1). Schedule 3 is organized by type of property: publicly traded shares, real estate, personal-use property, and other capital property. You'll list the proceeds of disposition, the ACB, and any outlays and expenses for each disposition.

The net capital gain (or loss) from Schedule 3 flows to line 12700 of your T1 return. If you have a net capital loss, it cannot be deducted against other income in the current year - but it can be carried back three years or carried forward indefinitely to offset future capital gains.

The Principal Residence Exemption

One of the most valuable tax benefits in Canada is the principal residence exemption (PRE). When you sell your home - the property you “ordinarily inhabited” during the years you owned it - the capital gain is completely tax-free. Each family unit (you, your spouse or common-law partner, and minor children) can designate one property as a principal residence for each tax year.

Even though the gain is exempt, you must still report the sale on your tax return using Schedule 3 and Form T2091. Failing to report can result in CRA denying the exemption entirely, which could mean a massive and unexpected tax bill. This is especially relevant for real estate investors who may own multiple properties and need to carefully plan which property to designate for each year.

Lifetime Capital Gains Exemption (LCGE)

If you sell qualified small business corporation (QSBC) shares, you may be eligible for the lifetime capital gains exemption. As of 2026, this exemption shelters up to $1,016,836 in capital gains from tax (the threshold is indexed to inflation annually). For qualified farm and fishing property, the exemption is even higher.

To qualify, the shares must meet specific conditions: the corporation must be a Canadian-controlled private corporation (CCPC) eligible for the small business deduction, at least 90% of its assets must be used in active business in Canada at the time of sale, and additional holding-period tests must be met. Proper planning well in advance of a sale is critical to ensure you meet all the criteria.

Capital Losses and How to Use Them

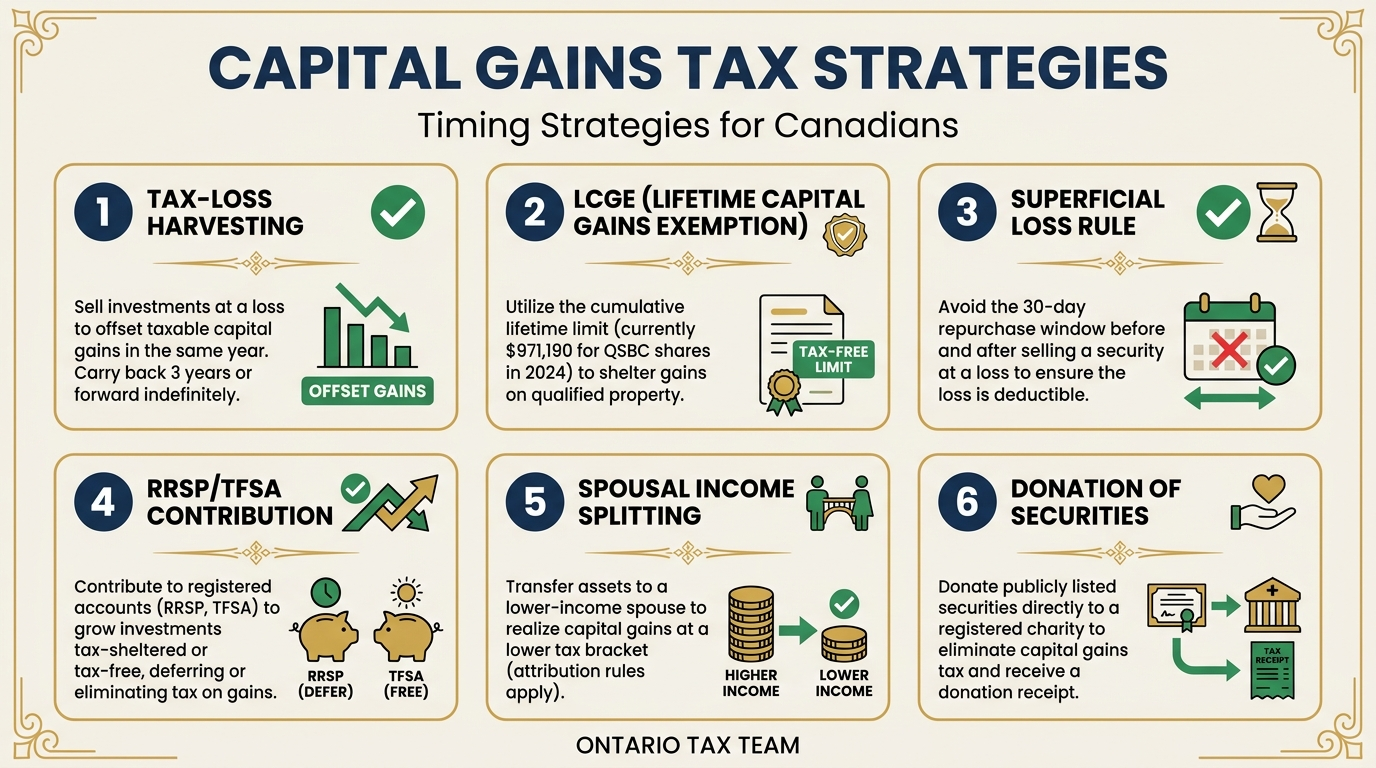

Capital losses are the flip side of capital gains. When you sell an asset for less than its ACB, you have a capital loss. Net capital losses can be applied against capital gains in the current year, carried back to any of the three preceding tax years, or carried forward indefinitely to offset future gains.

This makes year-end tax-loss harvesting a powerful strategy. If you have unrealized losses in your portfolio near the end of the year, you might sell those positions to crystallize the loss and offset gains realized earlier in the year. Just be careful of the superficial loss rule.

The Superficial Loss Rule

CRA's superficial loss rule prevents you from selling an asset to trigger a capital loss and then immediately repurchasing the same or identical asset. Specifically, if you (or a person affiliated with you, such as your spouse or a corporation you control) buy back the same property within 30 calendar days before or after the sale, the loss is denied. The denied loss is added to the ACB of the repurchased property, so it's not lost forever - it's just deferred until you eventually sell without triggering the rule again.

Timing Strategies for Capital Gains

Because capital gains are only taxed when you dispose of the property, you have some control over timing. Here are common strategies:

- Defer dispositions: If you expect to be in a lower tax bracket next year (for example, retiring or taking a sabbatical), consider delaying the sale to the following tax year. Use your RRSP contributions to offset the gain in the same year.

- Spread gains across years: If you're selling multiple assets, staggering the sales across two or more tax years can help you stay below the $250,000 threshold where the higher 66.67% inclusion rate kicks in.

- Use capital losses strategically: Harvest losses in the same year as large gains to reduce the net taxable amount.

- Consider the LCGE: If you're selling a business, structuring the transaction as a share sale rather than an asset sale may allow you to claim the lifetime exemption. Review when to incorporate if you haven't already.

- Gift to charity: Donating publicly listed securities directly to a registered charity eliminates the capital gains tax on those shares entirely, and you receive a donation tax credit.

If you own rental property in Ontario, be sure to review our guide on rental property tax deductions to understand how capital cost allowance (CCA) interacts with capital gains when you eventually sell.

Bottom Line

Capital gains tax in Canada is more nuanced than many people realize, and the 2025 changes to the inclusion rate add another layer of complexity for high-value dispositions. Whether you're selling an investment property, cashing out a stock portfolio, or planning the sale of your business, the decisions you make around timing, structure, and reporting can have a significant impact on your tax bill. Working with a qualified tax professional ensures you take advantage of every exemption and strategy available to you.

Key Takeaways

- •The first $250,000 in annual capital gains is included at 50%; amounts above that are included at 66.67% for individuals (effective June 25, 2025)

- •Your adjusted cost base (ACB) includes the purchase price plus acquisition costs and capital improvements

- •The principal residence exemption can eliminate tax on your home sale, but you must report it on your return

- •The LCGE can shelter over $1 million in gains on qualified small business shares

- •Watch for the superficial loss rule when tax-loss harvesting - a 30-day window applies

Need Help With Capital Gains Tax?

Our tax professionals help you minimize capital gains tax through strategic timing, exemptions, and proper reporting. Book a free 15-minute consultation.