If you own rental property in Ontario, you're entitled to deduct a wide range of expenses from your rental income, reducing the amount of tax you owe. But knowing which expenses are deductible - and which are not - is crucial for staying on the right side of the CRA while keeping your tax bill as low as legally possible.

This guide covers every major deduction available to Ontario landlords in 2026, how to report them on your tax return, and the record-keeping habits that will protect you if the CRA comes knocking.

How Rental Income Is Taxed in Canada

Rental income in Canada is reported on your personal tax return using Form T776, Statement of Real Estate Rentals. For a step-by-step walkthrough of this form, see our guide on how to report rental income in Canada. Your net rental income (gross rent minus allowable expenses) is added to your other income and taxed at your marginal tax rate. Unlike employment income, there are no CPP contributions on rental income, but it is still subject to both federal and Ontario provincial income tax.

Rental income is generally considered passive income. This matters because you cannot use rental losses to offset other types of income if the CRA determines you have no reasonable expectation of profit - though in most legitimate landlord situations, losses are fully deductible.

Deductible Rental Expenses on the T776

The CRA allows you to deduct any reasonable expense you incur to earn rental income. Here are the most common deductions landlords claim on their tax return:

Mortgage Interest

You can deduct the interest portion of your mortgage payments on a rental property. This is often the single largest deduction for landlords. Note that only the interest is deductible - the principal repayment is not, because paying down your mortgage is building equity, not covering an expense.

Property Taxes

Municipal property taxes on your rental property are fully deductible. In Ontario, property tax rates vary significantly by municipality, so this can be a substantial deduction depending on where your property is located.

Insurance Premiums

Premiums for property insurance, liability insurance, and landlord-specific coverage are deductible. If you have a policy that covers both your rental property and personal residence, only the portion attributable to the rental property qualifies.

Repairs and Maintenance

Expenses for maintaining or restoring a rental property to its original condition are deductible in the year they're incurred. This includes plumbing repairs, painting, replacing broken fixtures, and fixing appliances. However, improvements that enhance the property beyond its original condition (like a kitchen renovation or adding a deck) are considered capital expenditures and must be depreciated over time using CCA.

Advertising

Costs for advertising your rental vacancy - whether on rental listing websites, newspapers, or signage - are fully deductible.

Property Management Fees

If you hire a property manager to handle tenant relations, rent collection, and maintenance coordination, their fees (typically 5% to 10% of gross rent) are deductible. This is especially common for landlords who own multiple properties or live far from their rental.

Utilities

If you pay for heat, hydro, water, or internet for your rental property, those costs are deductible. If the tenant pays utilities directly, there's nothing for you to claim.

Other Deductible Expenses

- Legal and accounting fees: Fees paid for preparing your rental income tax return, lease agreements, or eviction proceedings

- Office supplies: Costs related to managing your rental (postage, stationery, bookkeeping software)

- Travel expenses: Mileage driven to collect rent, inspect the property, or meet with contractors (at the CRA's prescribed rate)

- Landscaping and snow removal: If you're responsible for maintaining the property exterior

- Condo fees: If your rental is a condo unit, the monthly maintenance fees are deductible

Capital Cost Allowance (CCA)

CCA is the tax equivalent of depreciation. It allows you to deduct a portion of the cost of your rental building and certain equipment (appliances, furniture) over several years. Rental buildings typically fall under CCA Class 1 at a rate of 4% per year (declining balance method).

While claiming CCA can reduce your taxable rental income, it also reduces your property's adjusted cost base. This means you'll pay more capital gains tax when you eventually sell. Many accountants recommend being cautious with CCA - only claim it if you expect to be in a higher tax bracket now than when you sell, or if you need the deduction to avoid a large tax bill. Talk to your accountant before claiming CCA on a property you plan to sell within the next few years.

Non-Deductible Items

Not everything you spend on your rental property is deductible. The most common non-deductible expenses include:

- Mortgage principal repayments: These reduce your debt, not your income

- Personal-use expenses: If you use part of the property yourself, you can only deduct the portion related to the rental use

- Land transfer tax: This is a capital cost, not a current expense (it gets added to your cost base)

- Value of your own labour: You cannot deduct the value of work you personally do on the property

Passive Income Rules and CCPC Implications

If you hold rental properties inside a Canadian-controlled private corporation (CCPC), be aware that rental income is considered passive investment income. Passive income above $50,000 per year reduces your access to the small business deduction, and passive income inside a corporation is taxed at a higher rate than active business income. For many landlords, holding properties personally or through a partnership is more tax-efficient, though the right structure depends on your overall financial picture.

If you own multiple rental properties or are considering incorporating your rental portfolio, get professional advice to weigh the trade-offs.

Principal Residence Exemption

If you convert your principal residence into a rental property, you can elect under section 45(2) of the Income Tax Act to defer the deemed disposition. This election lets you treat the property as your principal residence for up to four additional years, even after you stop living in it, which can shield capital gains on the property during that period.

The rules are nuanced - you cannot claim the principal residence exemption and CCA on the same property at the same time. If you've claimed CCA, the section 45(2) election is not available.

Capital Gains When You Sell

When you sell a rental property, any profit is treated as a capital gain. In Canada, two-thirds of the capital gain is included in your taxable income for 2026. The gain is calculated as the selling price minus your adjusted cost base (original purchase price plus legal fees, improvements, and land transfer tax, minus any CCA claimed).

Proper tracking of your cost base from day one is essential. Every improvement, every legal fee, and every CCA claim affects the calculation. Our personal income tax team can help ensure you report the disposition correctly and minimize your tax liability.

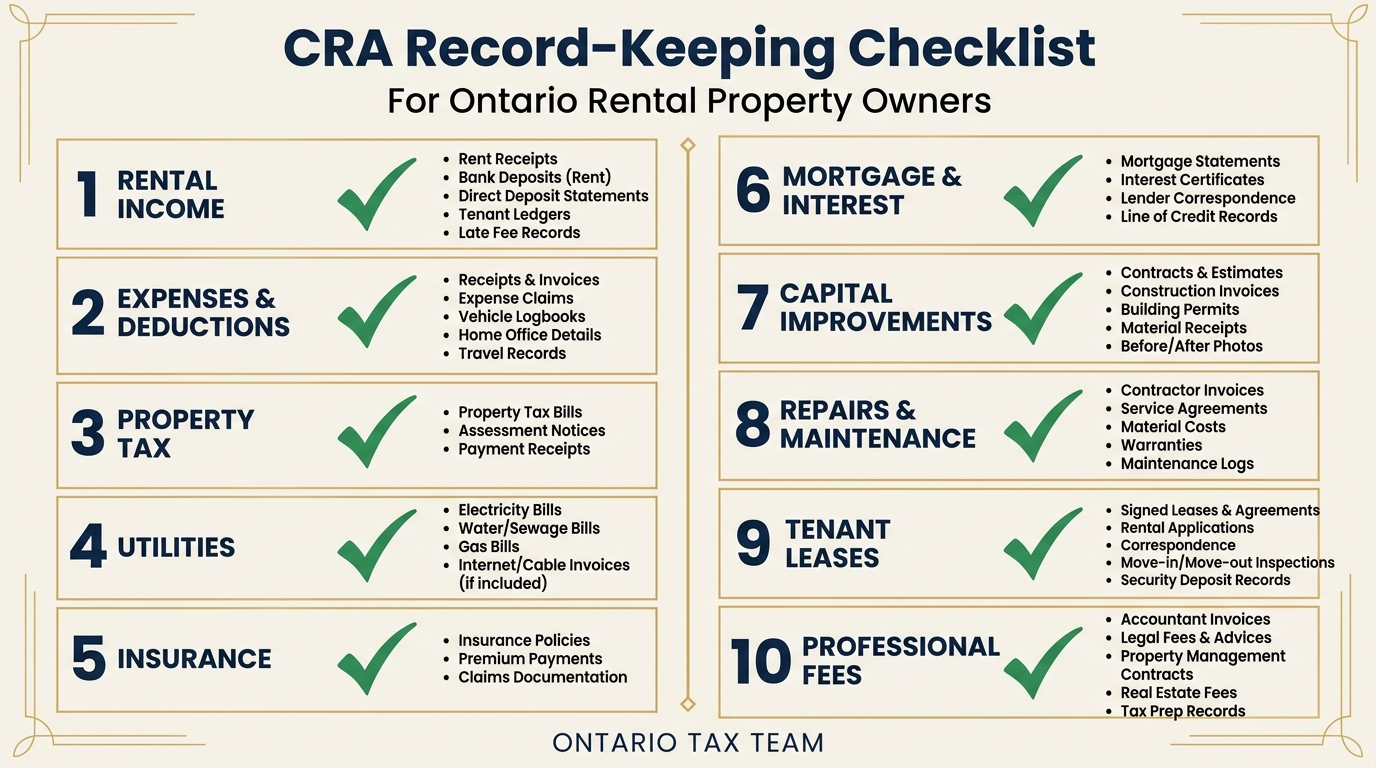

Record-Keeping Requirements

The CRA requires landlords to keep records for at least six years from the end of the tax year to which they relate. You should maintain:

- All receipts for expenses claimed as deductions

- Lease agreements and tenant correspondence

- Mortgage statements showing the interest-principal split

- Property tax assessments and payment records

- Records of all capital improvements (with dates and costs)

- A vehicle log if you claim travel expenses related to your rental

Using a cloud-based bookkeeping systemto track rental income and expenses throughout the year makes tax time far easier and ensures you don't miss deductions or lose receipts.

Bottom Line

Ontario landlords have access to a generous range of tax deductions that can significantly reduce the tax on rental income. The key is knowing exactly what qualifies, keeping meticulous records, and making strategic decisions about items like CCA. Working with an experienced accountantensures you claim every dollar you're entitled to without triggering CRA issues down the road.

Key Takeaways

- •Report rental income on Form T776 and deduct all reasonable expenses incurred to earn that income

- •Mortgage interest, property taxes, insurance, repairs, and management fees are all deductible - mortgage principal is not

- •Be cautious with CCA claims - they reduce your cost base and increase capital gains tax on sale

- •Keep all rental records for at least six years in case of a CRA audit

- •Get professional advice before incorporating a rental portfolio or claiming the principal residence exemption

Need Help With Rental Property Taxes?

Our tax team helps Ontario landlords maximize deductions and report rental income correctly. Book a free 15-minute consultation.