Earning rental income from a property in Canada? You're required to report it on your personal tax return every year, whether the property generated a profit or a loss. The CRA uses Form T776, Statement of Real Estate Rentals, to capture all the details - and getting it right matters for avoiding reassessments and penalties.

This guide walks you through the T776 step by step, from calculating gross rental income to claiming expenses and making smart decisions about capital cost allowance.

Step 1: Determine Your Gross Rental Income

Gross rental income is the total rent you received (or were entitled to receive) during the calendar year. This includes:

- Monthly rent payments from tenants

- Advance rent or last month's rent deposits (reported in the year received)

- Lease cancellation payments

- Any goods or services received from a tenant in lieu of rent (valued at fair market value)

If your property was vacant for part of the year, you still report only the rent actually received. However, you can typically continue claiming expenses during vacancy periods, as long as the property was available for rent and you were actively seeking tenants.

Step 2: Calculate Your Allowable Expenses

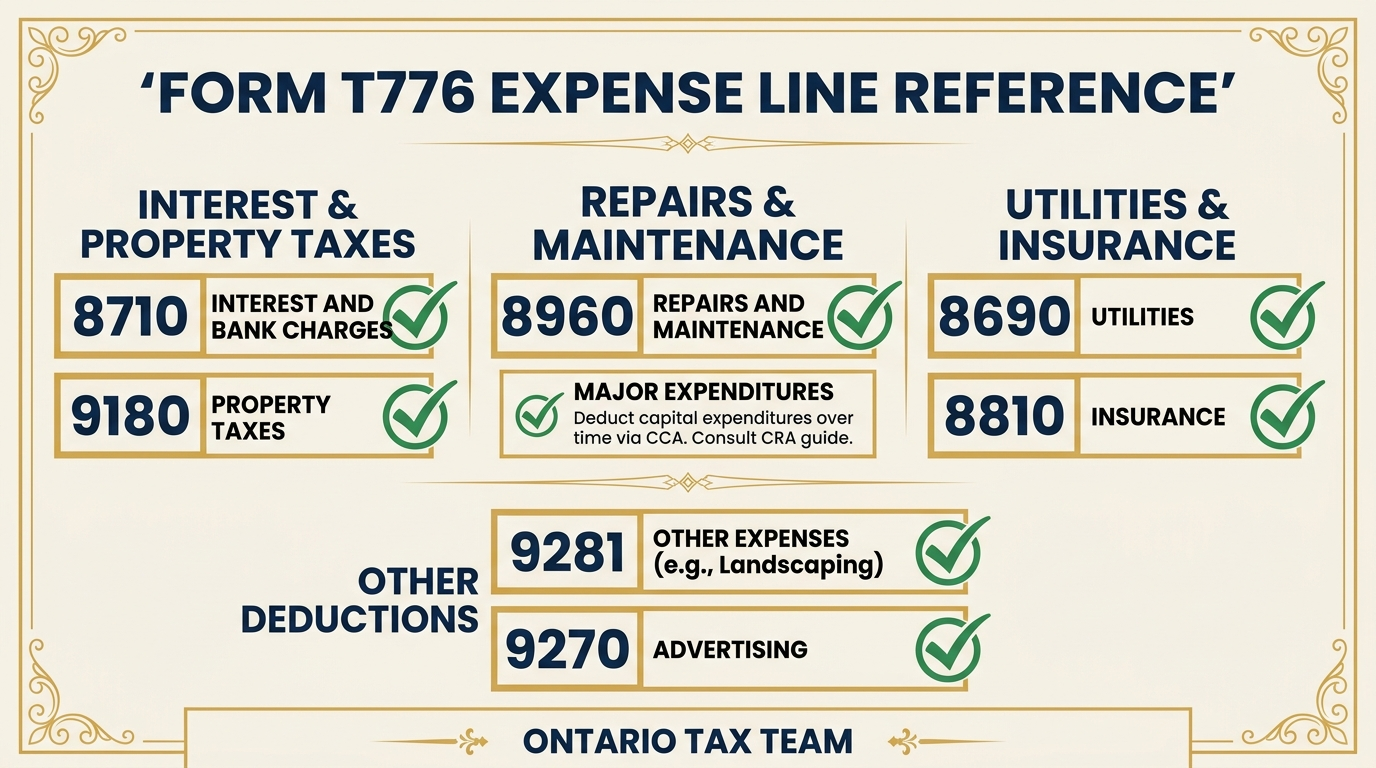

The T776 lists expense categories where you can claim costs incurred to earn rental income. For a detailed breakdown of every deductible expense, see our comprehensive guide to rental property tax deductions in Ontario. The major categories on the T776 include:

- Line 8810 - Advertising: Costs to advertise your rental vacancy

- Line 8811 - Insurance: Property and liability insurance premiums

- Line 8840 - Interest and bank charges: Mortgage interest and any financing costs

- Line 8860 - Professional fees: Accounting, legal, and property management fees

- Line 8871 - Maintenance and repairs: Costs to maintain the property in its current condition

- Line 8910 - Property taxes: Municipal property taxes

- Line 8960 - Utilities: Heat, hydro, water, internet (if paid by you)

Total your expenses and subtract them from gross rental income. If expenses exceed income, you have a rental loss.

Step 3: Decide Whether to Claim CCA

Capital cost allowance lets you deduct a portion of the cost of your rental building and depreciable assets (appliances, furniture, equipment) each year. For rental buildings acquired after November 2018, the standard rate is 4% per year under CCA Class 1, and the Accelerated Investment Incentive may allow a higher first-year deduction.

There's an important strategic decision here: CCA is optional, and many experienced landlords choose not to claim it. Here's why:

- CCA reduces your adjusted cost base. When you sell, your capital gain will be larger because your cost base is lower. In some cases, the CCA previously claimed is “recaptured” and taxed as regular income.

- CCA cannot create or increase a rental loss. You can only claim CCA up to the point where your net rental income reaches zero. You can't use CCA to generate a loss that offsets other income.

- It complicates the principal residence exemption. If you claimed CCA on a property that was previously your home, you lose the ability to make the section 45(2) election.

Claim CCA only if the immediate tax savings are worth the future cost, or if you don't plan to sell the property for a long time. Your accountant can model the numbers for your specific situation.

Step 4: Complete the Property Details

The T776 requires you to provide the property address, the number of units, your ownership percentage, and the year you acquired the property. If you own the property jointly with a spouse or partner, each person files their own T776 reporting their share of the income and expenses based on ownership percentage.

Step 5: Reporting Co-Owned Properties

If you co-own a rental property, each owner must report their share of rental income and expenses. For spouses, the CRA generally expects income to be split according to legal ownership. If you own 50% of the property, you report 50% of the income and 50% of the expenses. You cannot arbitrarily allocate more income to the lower-income spouse to save taxes - the CRA's attribution rules prevent this.

For non-spouse co-owners (business partners, family members), income and expenses are typically split according to the partnership agreement or the ownership registered on title.

Reporting a Rental Loss

If your allowable expenses (excluding CCA) exceed your gross rental income, you have a rental loss. In most cases, this loss can be deducted against your other income, reducing your overall tax bill. This is one of the advantages of real estate investing - interest, property taxes, and repair costs incurred during renovation or low-occupancy periods can generate tax savings even when cash flow is negative.

However, the CRA may challenge repeated rental losses if they believe the property has no reasonable expectation of profit - see our CRA audit guide for what triggers scrutiny. Maintain documentation showing your intent to earn rental income, including records of your efforts to find tenants, improve the property, and achieve positive cash flow.

First-Year Landlord Tips

If this is your first year reporting rental income, here are some practical tips to get started on the right foot:

- Open a separate bank account for your rental property. This makes tracking income and expenses dramatically easier and gives you a clean audit trail.

- Keep every receipt from day one. Digital copies are acceptable - use a scanner app on your phone and organize files by property and year. See our tax season document preparation guide for more tips.

- Track mileage for trips to the property. The CRA allows you to deduct vehicle expenses at the prescribed per-kilometre rate.

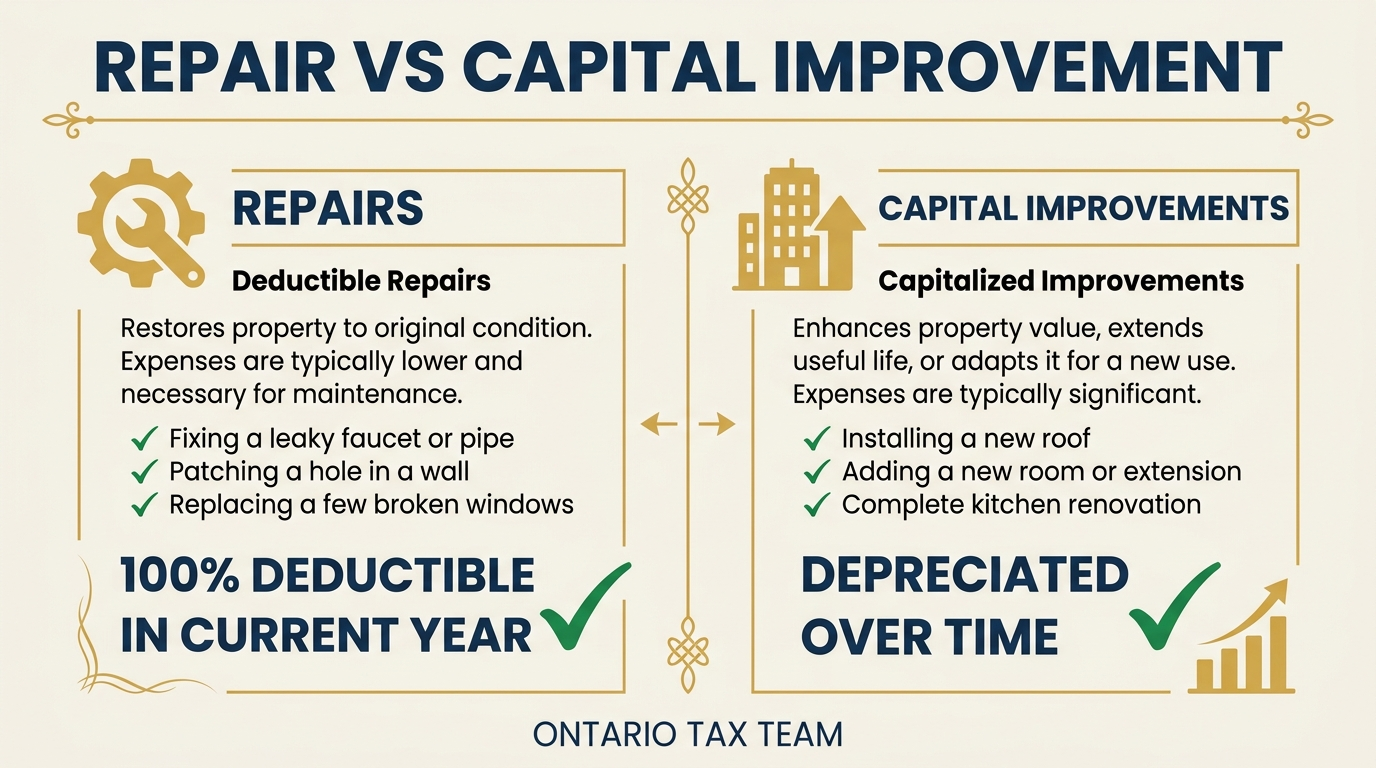

- Understand the repair vs. improvement distinction. A repair restores something to its original condition (deductible now). An improvement enhances it beyond original condition (capitalized and depreciated through CCA).

- Get professional help. The T776 is straightforward for a single property with simple expenses, but it gets complicated quickly with multiple properties, co-ownership, or significant capital improvements. Working with an accountant experienced in real estate saves you time and money.

CRA Requirements and Filing

You don't mail the T776 to the CRA separately - it's part of your T1 personal income tax return. If you e-file (which you should), the amounts from your T776 flow automatically to the correct lines on your return. The CRA can request your supporting documents at any time, so keep records for a minimum of six years.

For detailed information on the T776 form, the CRA publishes Guide T4036, “Rental Income,” which is available on the CRA website. Your personal income tax preparer can handle the entire T776 preparation as part of your annual filing.

Using Bookkeeping Software for Rental Properties

If you own one or more rental properties, tracking income and expenses in a spreadsheet becomes cumbersome fast. Cloud-based bookkeeping software like QuickBooks Online lets you categorize transactions, attach receipt images, run profit-and-loss reports by property, and export everything your accountant needs at tax time. The cost of the software is itself a deductible expense.

Bottom Line

Reporting rental income correctly is not optional - the CRA has access to property ownership records, land transfer data, and mortgage information. Getting the T776 right from the start protects you from reassessments and ensures you're claiming every deduction you're entitled to. Whether you have one rental unit or a growing portfolio, working with a professional who understands real estate taxation is one of the best investments you can make.

Key Takeaways

- •All Canadian rental income must be reported on Form T776 as part of your T1 return

- •CCA is optional and should be claimed strategically - it reduces your cost base and can trigger recapture on sale

- •Co-owned properties must be reported according to legal ownership percentage - you cannot split income arbitrarily

- •Rental losses are generally deductible against other income, but maintain documentation of your profit intent

- •Keep all records for at least six years and use a separate bank account for each rental property

Need Help Reporting Rental Income?

Our tax team handles T776 preparation and ensures every rental deduction is claimed correctly. Book a free 15-minute consultation.