There's a meaningful difference between tax preparation and tax planning. Tax preparation happens once a year when you file your returns. Tax planning happens year-round - and it's where the real savings are. If you're waiting until March or April to think about your tax bill, you've already missed most of the opportunities to reduce it.

This guide covers the key tax planning strategies available to small business owners in Ontario, from straightforward tactics anyone can use to more advanced structures that require professional guidance.

Year-Round Planning vs Year-End Scramble

The most effective tax strategies require action throughout the year, not just in December. Timing the purchase of equipment, managing the balance between salary and dividends, making RRSP contributions, and tracking expenses properly all require forward planning.

Work with your CPA or tax planning advisorto set a calendar of quarterly review meetings. These check-ins let you project your annual income, estimate your tax liability, and make strategic decisions while there's still time to act.

Income Splitting with Family Members

If your corporation pays dividends to family members who are shareholders, you can distribute income across multiple people in lower tax brackets. This reduces your family's overall tax burden because Canada's personal income tax system is progressive - the more you earn, the higher the rate.

However, the Tax on Split Income (TOSI) rules introduced in 2018 significantly restrict income splitting. Dividends paid to family members who don't meaningfully contribute to the business may be taxed at the top marginal rate. To benefit from income splitting legally, family shareholders generally need to be actively involved in the business, have contributed capital, or be over the age of 24 with certain qualifications. This is an area where professional advice is essential.

Source: Canada Revenue Agency, Ontario Ministry of Finance (2025 rates)

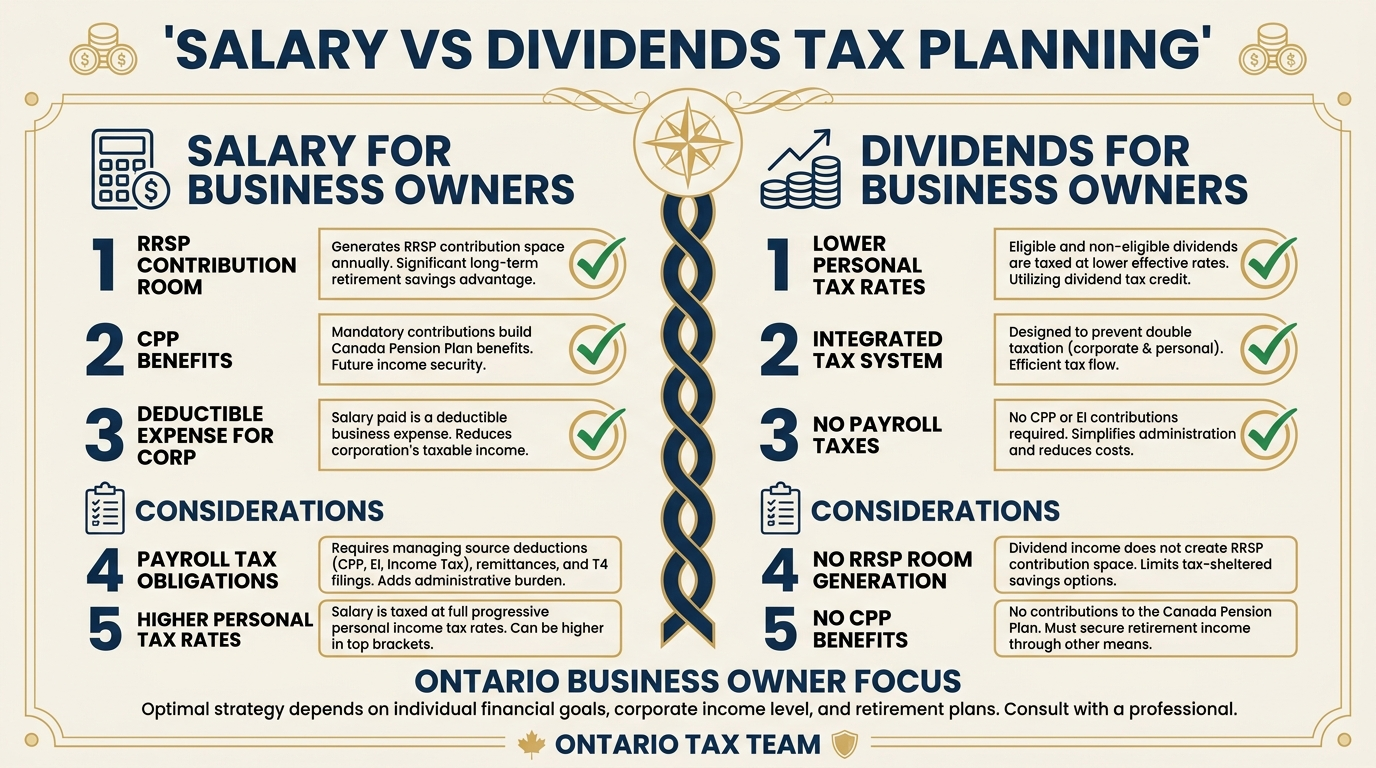

Salary vs Dividend Optimization

As a business owner with an incorporated company, you choose how to pay yourself - salary, dividends, or a combination of both. Each has different tax implications. For a comprehensive comparison, see our guide on salary vs dividends.

Salary Advantages

- Creates RRSP contribution room

- Is a deductible expense for the corporation, reducing corporate taxable income

- Contributes to CPP, which provides retirement and disability benefits

- Supports applications for mortgages and personal loans

Dividend Advantages

- No CPP contributions required (saving both employee and employer portions)

- Eligible dividends receive a tax credit that can result in lower personal tax on the same pre-tax corporate income

- Simpler to administer - no payroll, no T4 slips for the dividend portion

The optimal mix depends on your personal situation, income level, RRSP room, and whether you need CPP contributions. Most business owners benefit from a blend of both, adjusted annually based on projections.

Timing of Expenses

If your fiscal year-end is approaching and you have a strong profit, consider accelerating deductible expenses. Prepay rent, stock up on supplies, pay outstanding invoices to contractors, or renew annual subscriptions before year-end. These expenses reduce your corporate taxable income for the current year.

Conversely, if you expect next year to be more profitable, you might delay certain expenses to maximize their impact in a higher-income year. Strategic timing doesn't change what you spend - it changes when you get the tax benefit.

Asset Purchases Before Year-End

Capital assets like computers, vehicles, furniture, and equipment are deducted over time through Capital Cost Allowance (CCA). Under the Accelerated Investment Incentive, most assets purchased and available for use before your year-end can claim enhanced first-year depreciation.

If you're planning a significant equipment purchase in the near future, buying it before your fiscal year-end rather than after can provide a meaningful tax deduction in the current year. Just make sure the purchase makes business sense independent of the tax benefit - don't buy things you don't need just to reduce taxes.

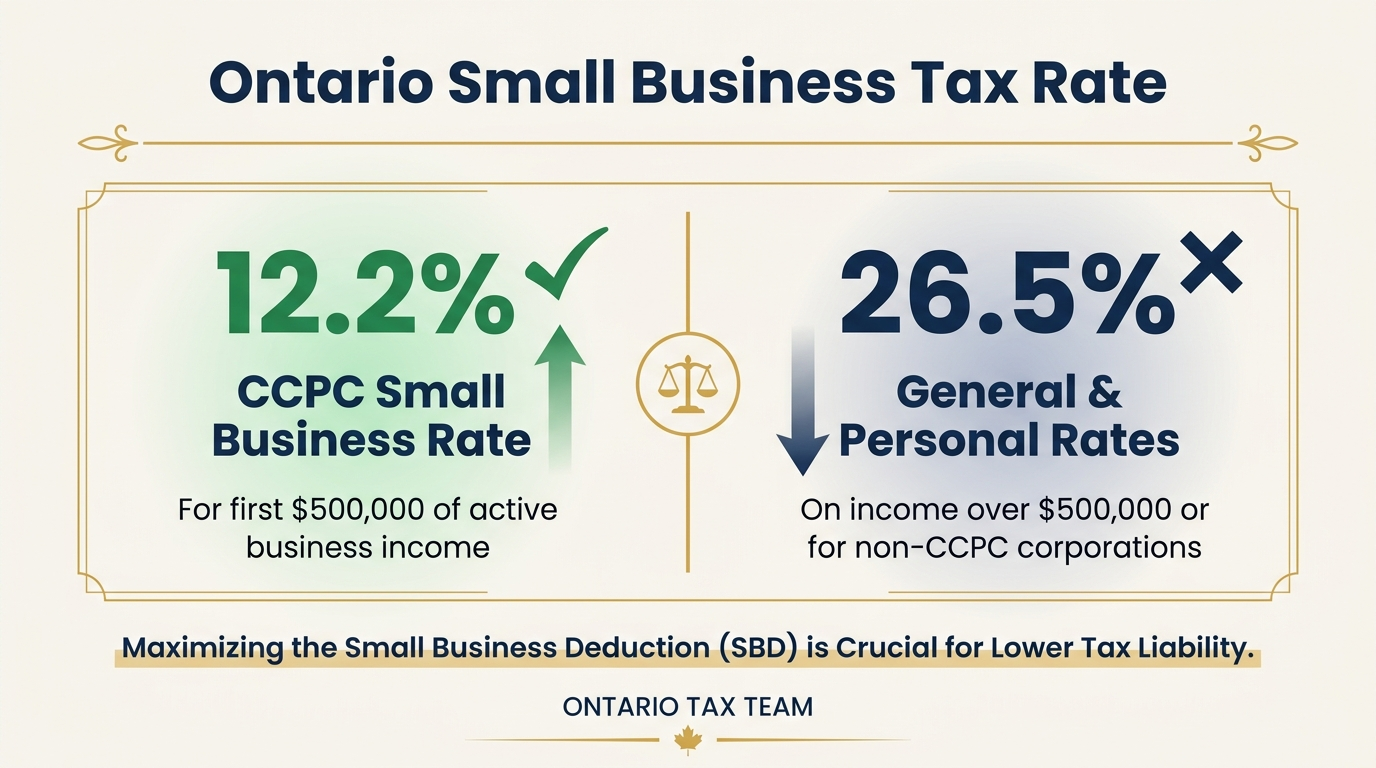

Small Business Deduction Optimization

The Small Business Deduction (SBD) allows Canadian-Controlled Private Corporations (CCPCs) to pay a combined federal-provincial tax rate of approximately 12.2% on the first $500,000 of active business income in Ontario. Above that threshold, the rate jumps to approximately 26.5%.

If your business income is approaching $500,000, strategies to stay within the SBD limit can be valuable. These include paying yourself a larger salary (which reduces corporate income) or timing revenue recognition. If you have associated corporations, be aware that the $500,000 limit is shared among them.

RRSP and IPP Contributions

If you pay yourself a salary, you build RRSP contribution room (18% of earned income, up to the annual maximum). RRSP contributions reduce your personal taxable income and grow tax-deferred until withdrawal. For business owners over 40 with consistent salary history, an Individual Pension Plan (IPP) can allow even larger tax-deductible contributions than an RRSP.

An IPP is a defined benefit pension plan set up for a single individual. The corporation makes the contributions, which are fully tax-deductible to the business and not taxable to the individual until benefits are received in retirement. IPPs are particularly effective for incorporated professionals and business owners with stable, high incomes.

Holding Company Structures

A holding company (holdco) is a separate corporation that owns shares in your operating company (opco). There are several strategic advantages to this structure:

- Asset protection: Profits moved to the holdco are sheltered from the operating company's liabilities

- Tax deferral: Dividends can flow between connected Canadian corporations tax-free through the inter-corporate dividend mechanism

- Estate planning: A holdco can facilitate an estate freeze, locking in the current value of your business for tax purposes

- Investment flexibility: Surplus cash in the holdco can be invested without exposing it to operational risks

Setting up and maintaining a holding company involves legal and accounting costs, so it's typically worthwhile only when your operating company consistently generates surplus profits beyond what you need for operations and personal compensation.

Shareholder Loans

If you borrow money from your corporation, CRA treats the loan as taxable income unless it's repaid within one year of the corporation's fiscal year-end. Shareholder loan rules are strict and the consequences of getting them wrong are severe - the full loan amount gets added to your personal income.

If you need to take money out of your corporation beyond salary and dividends, plan carefully with your accountant. There are legitimate ways to structure shareholder loans, but they require careful documentation and timely repayment.

Capital Dividend Account

When your corporation realizes a capital gain, only 50% is taxable. The non-taxable portion accumulates in the corporation's Capital Dividend Account (CDA). You can pay tax-free dividends to shareholders from this account, making it one of the most efficient ways to extract money from your corporation.

The CDA also receives life insurance proceeds (net of the policy's adjusted cost basis), making corporate-owned life insurance a powerful estate planning tool. Tracking and using your CDA balance requires careful record-keeping and proper CRA filings.

Working with a CPA

The strategies outlined above range from straightforward to highly complex. Implementing them incorrectly can result in unexpected tax bills, CRA penalties, or loss of preferred tax rates. Keeping accurate bookkeepingrecords is the foundation for every strategy listed here. A qualified CPA who understands Ontario's tax landscape can model different scenarios, project outcomes, and help you make decisions that optimize your overall tax position.

Ontario Tax Team's corporate tax and tax planning services are designed specifically for small business owners who want to be proactive about their taxes rather than reactive. We work with you throughout the year - not just at filing time - to ensure every available strategy is on the table.

Bottom Line

Tax planning is not a one-time event. It's an ongoing process that requires regular attention and professional guidance. Use our tax calculator to model different income scenarios. The most tax-efficient business owners in Ontario are the ones who plan proactively, review their position quarterly, and make strategic decisions about salary, dividends, expenses, and corporate structures well before their year-end. Start early, stay consistent, and work with a CPA who understands your goals.

Key Takeaways

- •Year-round tax planning saves significantly more than year-end scrambling

- •The salary vs dividend mix should be optimized annually based on your personal situation

- •The Small Business Deduction provides a 12.2% tax rate on the first $500,000 of active business income in Ontario

- •Holding companies, IPPs, and Capital Dividend Accounts offer advanced tax efficiency for profitable businesses

- •Work with a CPA quarterly to project income and implement strategies while there's still time

Need Help With Tax Planning?

Our tax planning team works with Ontario small businesses year-round to minimize taxes and maximize growth. Book a free 15-minute consultation.