Good bookkeeping isn't just about staying compliant with CRA - it's the foundation of every smart financial decision you make as a business owner. Yet many entrepreneurs treat bookkeeping as an afterthought, scrambling at year-end to piece together a full year's worth of transactions. That approach leads to missed deductions, inaccurate financial statements, and unnecessary stress.

Whether you handle your own books or work with a professional bookkeeping service, these ten tips will help you keep your finances clean, organized, and ready for anything.

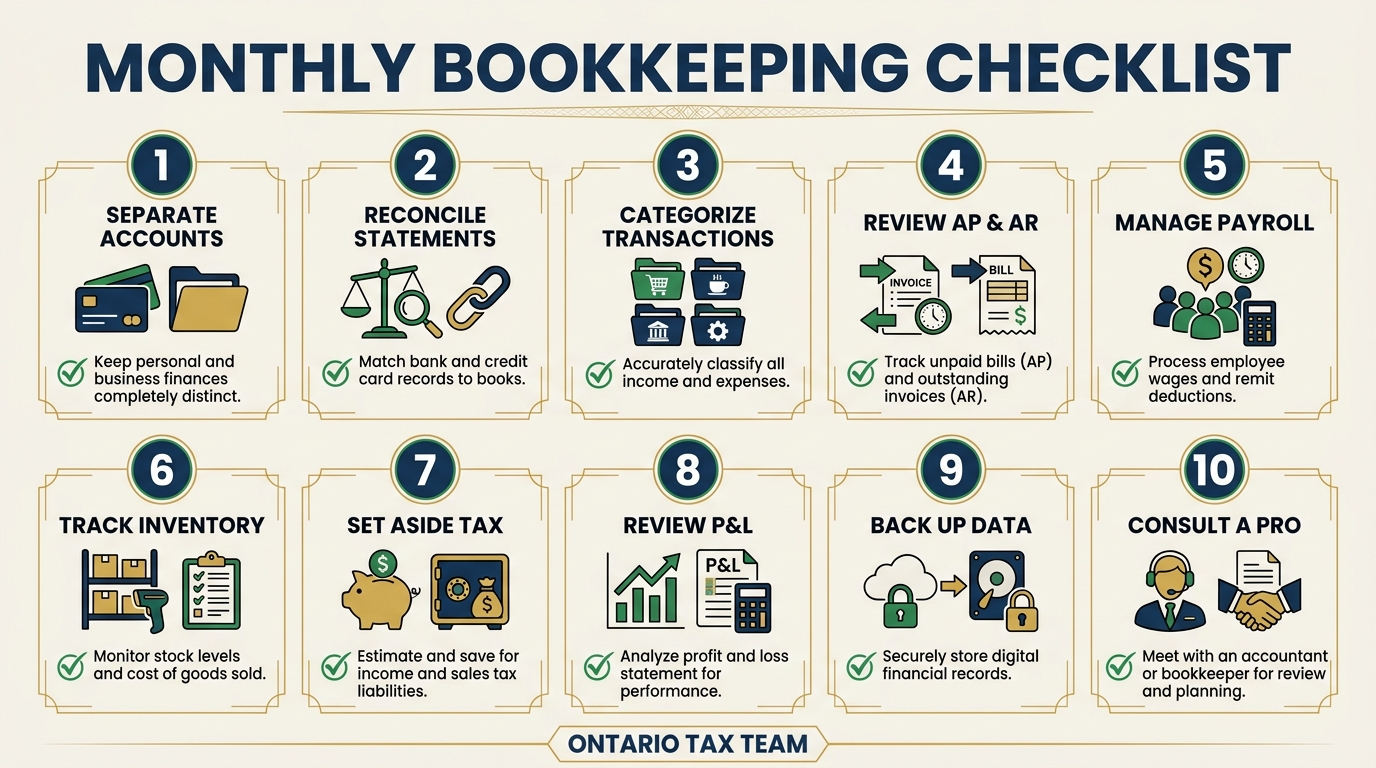

1. Separate Your Business and Personal Accounts

This is the single most important step you can take. Open a dedicated business bank account and a business credit card. Run every business transaction through those accounts and nothing else. When personal and business expenses are mixed together, it becomes nearly impossible to track profitability accurately, and it creates a nightmare at tax time.

If CRA ever audits your business, commingled accounts raise immediate red flags. A clean separation makes it straightforward to prove which expenses are legitimate business costs and which are personal.

2. Reconcile Your Accounts Monthly

Bank reconciliation means comparing your bookkeeping records against your actual bank and credit card statements to make sure they match. This should happen every month without exception. Monthly reconciliation catches errors, identifies missing transactions, and detects unauthorized charges before they become bigger problems.

If you let reconciliation slide for several months, the catch-up process becomes exponentially harder. What takes thirty minutes per month can turn into days of work when left for a full year.

3. Track and Digitize Your Receipts

CRA requires you to keep supporting documentation for every business expense you claim. Paper receipts fade, get lost, or end up crumpled at the bottom of a drawer. Use a receipt scanning app or your accounting software's built-in capture feature to photograph receipts immediately after each purchase.

Store digital copies organized by month or category. This habit takes seconds per transaction but saves hours when you need to substantiate deductions during tax filing or a CRA review.

4. Categorize Expenses Properly

Every expense should be assigned to the correct category in your chart of accounts - office supplies, advertising, professional fees, meals and entertainment, vehicle expenses, and so on. Proper categorization ensures your financial statements are meaningful and your tax return captures every available deduction.

Avoid the temptation to dump miscellaneous expenses into a catch-all category. If “Other Expenses” is one of your largest line items, your chart of accounts needs work. For a detailed list of what you can claim, see our guide on small business tax deductions in Canada.

5. Use Cloud-Based Accounting Software

Spreadsheets have their place, but once your business has any meaningful transaction volume, dedicated cloud accounting software is essential. Platforms like QuickBooks Online, Xero, or FreshBooks connect directly to your bank accounts, automate transaction imports, generate financial reports, and make it easy to collaborate with your bookkeeper or accountant.

Cloud software also means your data is backed up automatically and accessible from anywhere. If you're running a small business in Ontario, having real-time access to your financial data helps you make faster, better-informed decisions.

6. Review Your Profit and Loss Statement Monthly

Your profit and loss statement (also called an income statement) - one of the key financial statements- summarizes your revenue, expenses, and net profit for a given period. Reviewing it monthly gives you a pulse on how your business is actually performing - not how you think it's performing.

Look for trends: Is a particular expense category growing faster than revenue? Are seasonal patterns consistent with last year? Are there any unexpected charges? Monthly P&L reviews help you spot problems early and make adjustments before they compound.

What to Look for in Your Monthly P&L

- Gross profit margin - is it holding steady or declining?

- Operating expenses as a percentage of revenue

- Any new or unusual expense line items

- Revenue trends compared to the same period last year

- Net profit - are you actually making money after all expenses?

7. Stay on Top of HST

If your business earns more than $30,000 in revenue over four consecutive quarters, you're required to register for HST. Once registered, you collect HST on your sales and remit it to CRA, minus any Input Tax Credits (ITCs) for HST paid on business expenses.

The key mistake small business owners make is treating collected HST as revenue rather than a liability. That money belongs to CRA, not to you. Track HST collected and paid separately, and set it aside in a dedicated account so you're never caught short when the filing deadline arrives.

8. Keep Records for at Least Six Years

CRA requires you to retain all business records and supporting documents for a minimum of six years from the end of the tax year they relate to. This includes invoices, receipts, bank statements, contracts, payroll records, and tax returns.

Digital storage makes this easy. Maintain organized folders by year, and back them up in at least two locations. If CRA requests records from three years ago - during a CRA audit, for example - you need to be able to produce them promptly.

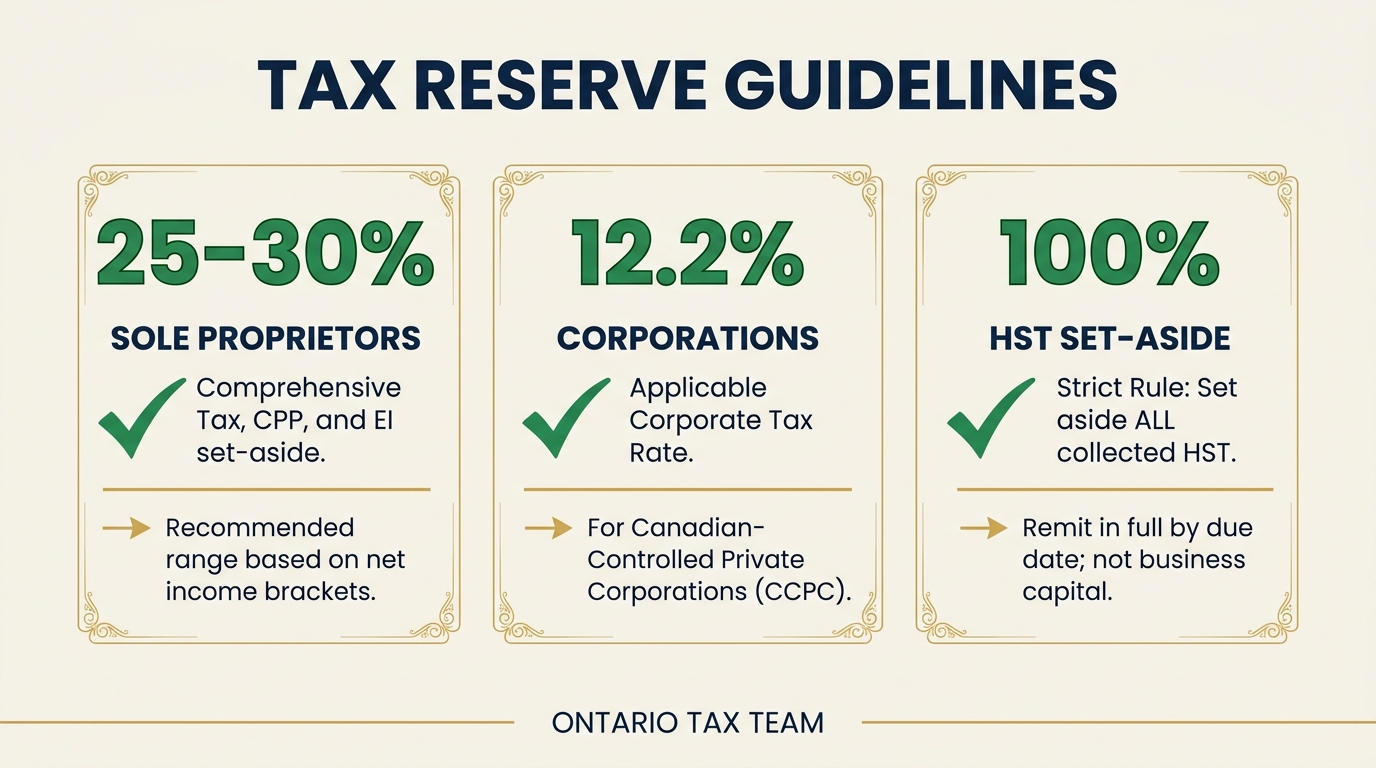

9. Set Aside Money for Taxes

One of the most common cash flow crises small businesses face is an unexpected tax bill. Whether it's income tax, HST, or payroll remittances, taxes are a predictable expense - so plan for them.

A good rule of thumb is to set aside 25% to 30% of your net income for combined federal and provincial income taxes. Open a separate savings account for tax reserves and transfer money into it regularly. When tax payments come due, the money is already there.

Tax Reserve Guidelines

- Sole proprietors: Set aside 25-30% of net self-employment income

- Incorporated businesses: The small business rate in Ontario is approximately 12.2%, but personal taxes on dividends or salary add more

- HST: Keep collected HST in a separate account - it's not your money

- Payroll: Remit on time to avoid penalties - CRA is strict about payroll deadlines

10. Hire Help When You're Overwhelmed

There's no prize for doing everything yourself. If bookkeeping is eating into time you should be spending on sales, client work, or operations, it's time to bring in a professional. The cost of a virtual bookkeeping serviceis almost always less than the value of the time you're spending on it - and a professional will do it more accurately.

Even if you're not ready for full-service bookkeeping, consider having a professional set up your chart of accounts, establish your processes, and train you on best practices. A strong foundation makes everything easier going forward.

Bottom Line

Clean, consistent bookkeeping isn't glamorous, but it's what separates businesses that thrive from businesses that operate in the dark. These ten habits take relatively little time when practiced consistently, and they pay dividends in accurate tax filings, better financial decisions, and peace of mind.

If your books need attention, Ontario Tax Team's bookkeeping team can help - whether you need monthly maintenance, catch-up work, or a complete setup from scratch. For a deeper look at how bookkeeping and accounting work together, read our guide on bookkeeping vs accounting.

Key Takeaways

- •Always keep business and personal finances completely separate

- •Reconcile bank accounts monthly and review your P&L regularly

- •Digitize receipts immediately and keep records for at least six years

- •Set aside 25-30% of net income for taxes so you're never caught off guard

- •Hire a professional bookkeeper when bookkeeping starts taking time away from growing your business

Need Help With Your Bookkeeping?

Our bookkeeping team keeps your books clean, accurate, and CRA-ready so you can focus on running your business. Book a free 15-minute consultation.